Trading professionals may find and seize chances in the stock market by understanding how to appropriately assess a company. The foundation for traders to determine whether a company is reasonably cheap or costly is provided by stock valuation, often known as “equity valuation” Traders have the potential to profit from the discrepancy between a stock’s market value and intrinsic value.

WHY SHOULD YOU VALUE A STOCK?

By valuing a stock, traders may get a thorough grasp of a share’s worth and determine if its price is reasonable. Once the share’s worth is understood, it may be contrasted with the share’s stock market quoted price.

Traders will try to short/sell the stock if the quoted share price exceeds the estimated value because they perceive it to be overvalued and anticipate the price returning to its intrinsic value.

It is considered cheap if the listed price is less than the calculated price, and traders would try to purchase or go long the stock in the hope that the price will eventually return to its intrinsic value.

The following details sum up this relationship:

Market value > intrinsic value = Overvalued (short signal)

Market value < intrinsic value = Undervalued (long signal)

It is important to note that even if a stock may be overpriced or undervalued, it may stay that way for a while if the imbalance’s underlying reason continues.

THE VARIOUS TYPES OF STOCK VALUE

What establishes a stock’s value? The easiest approach to respond to this is to discuss the idea of worth. Value: What is it? Is it the price that one buyer is willing to accept from another (market value) or is it an inherent worth that can be determined objectively based on a set of publically accessible data?

The following definitions of these two ideas:

1) Market value: The share price quoted on the stock market. The latest traded price is what it is. A willing buyer and a willing seller will trade goods at a price known as market value.

2) Intrinsic value: A more measured evaluation of worth based on data that is readily accessible to the public. Since there is no established formula for valuing stocks, experts often arrive at various intrinsic values, yet, these values often only vary a little.

Share prices very often diverge from their fundamental worth. A situation with a lot of anticipation about a new share or one that is expanding swiftly and investors looking to buy it soon would be an illustration of this. Growing FOMO would logically extend this mismatch until there is a significant decline in the share price.

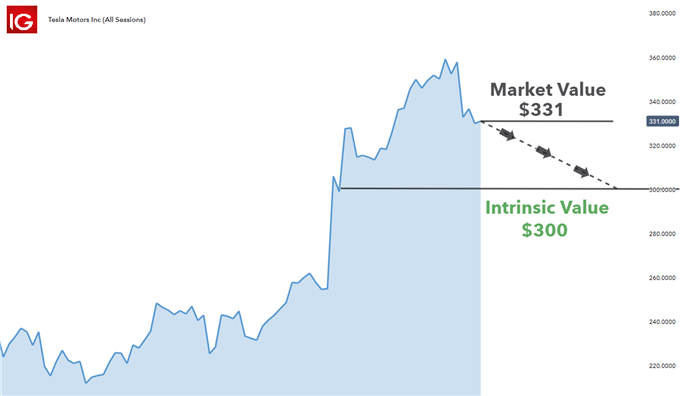

Traders may expect a move down near $300, for instance, if Tesla Inc. is presently trading at $331 and has an intrinsic value of $300.

An example of a stock trading above its intrinsic value is Tesla Inc.

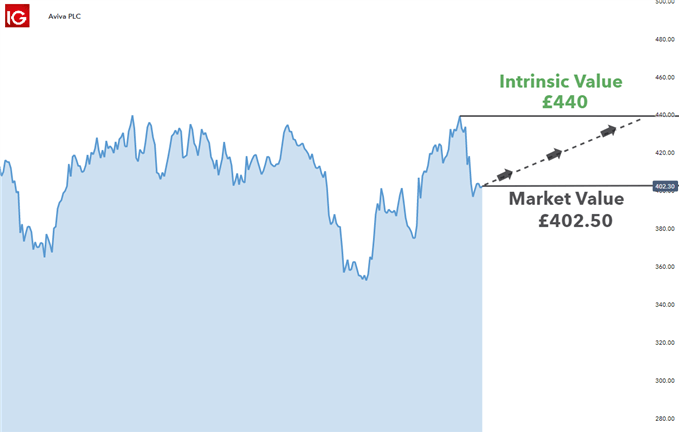

The opposite is also true when investors buy shares of a company when they are trading below their intrinsic value in the hopes that the price would rise to reflect the inherent worth. Value stocks often operate in this manner. In the scenario below, Aviva PLC is trading below its intrinsic value.

Aviva PLC is a good illustration of a company selling below its actual value.

THE TOP 3 WAYS TO DETERMINE A STOCK’S VALUE

Leading financial institutions and hedge fund managers undertake stock valuation using extremely complex variants of the procedures below. This article aims to provide investors with a thorough starting point for stock valuation for the following stock valuation methods:

P/E Ratio

PEG Ratio

Dividend Discount Model (DDM)

- The P/E Ratio

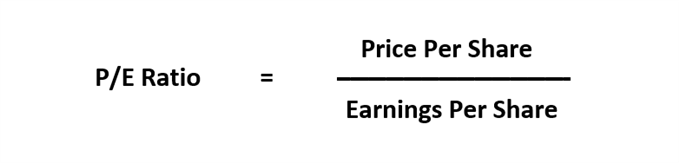

One of the most often used methods of valuing a share is the price-to-earnings ratio, or P/E ratio, widely used by investing experts.

Instead of providing an intrinsic value, the ratio compares the company’s P/E ratio to a benchmark, such as other businesses in the same industry, to see if the stock is comparatively overpriced or undervalued.

The stock price per share is subtracted from the earnings per share to arrive at the P/E ratio.

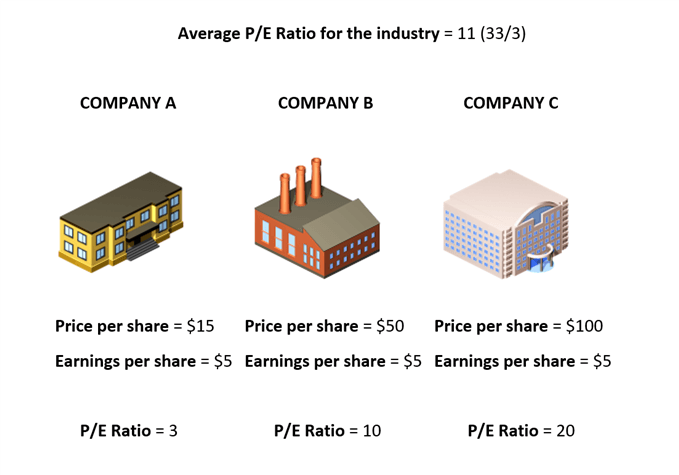

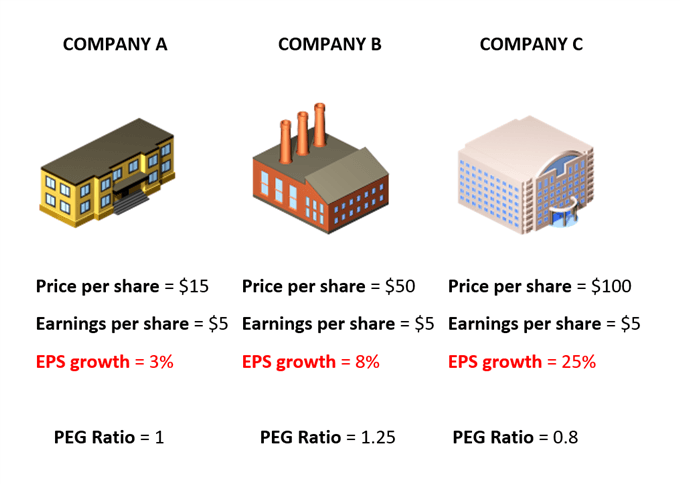

Think about, for instance, the three following businesses and their different P/E ratios:

Being below the industry average of 11, Companies A and B seem appealing. This serves as the foundation for stock valuation since there can be a very solid reason why these businesses seem to be undervalued. It’s conceivable that the business has taken on too much debt, and the share price appropriately represents the debt-ridden company’s market worth.

Company C, which has a P/E ratio that is well above average, requires the same amount of research. While it seems pricey, likely, the market has already factored in higher future profits growth, and investors are thus prepared to pay more for these higher earnings.

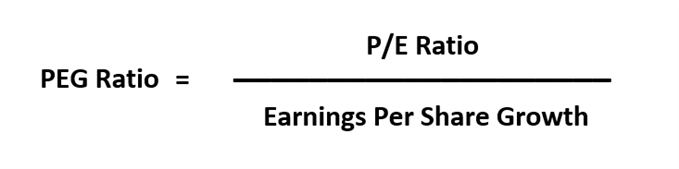

- The PEG Ratio

Traders can determine the value of a company by extending the P/E ratio and factoring in the Earnings Per Share growth rate (EPS). This is more accurate since profits are seldom static, and by including EPS growth in the equation, a more dynamic stock value model is produced.

A historical earnings number may be used to get a “Trailing PEG” or an anticipated figure can be used to calculate a “Forward PEG.”

This is how the PEG ratio is determined:

The formula for valuing stocks:

Take the same illustration but add information about profits growth:

Generally, a PEG ratio of less than one indicates a solid investment. In contrast, ratios greater than one indicate that the stock’s current price is too expensive compared to its expected profit growth and, as a result, is not a good bargain.

The PEG ratios show that Company A is OK, Company C is quite alluring despite its high price, and Company B does not seem flattering.

It’s important to reiterate that investing selections shouldn’t be based just on PEG ratios and that further research into the company’s financial statements should be done.

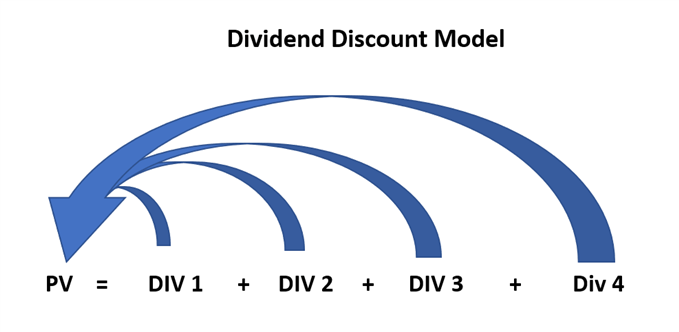

- DIVIDEND DISCOUNT MODEL (DDM)

As it considers future dividends (profits) to shareholders, the dividend discount model is comparable to the earlier stock valuation techniques. To determine what those dividends would be worth in today’s value, sometimes known as the present value, the DDM model, however, looks at future payouts and discounts them (PV).

This is justified by the idea that the value of the share today should correspond to the number of dividends the shareholder would ultimately receive, discounted to the present.

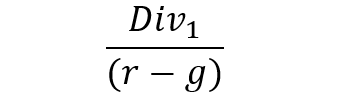

Assume a dividend payment is made once per year to make the computation easier. Furthermore, it is common to anticipate that dividends would rise over time as the company expands and as a consequence of inflationary impacts. Larger profitability and, thus, increased dividend payments result from higher input costs that are passed down to consumers.

Assuming constant growth, the dividend growth is shown below by the letter “g.” Future cash flows are discounted to today’s value using the needed rate of return, or r.

The formula for stock valuation:

- PV = Stock’s present value

- DIV1 = Dividend expected one year from now

- r = Discount rate

- g = Constant dividend growth

Dividends paid out in the future have less worth in terms of today’s value, which lowers their contribution to the stock’s current value. The stock value determined by the dividend discount model is the answer at PV after future dividends have been discounted.

KEY TAKEAWAYS FROM DETERMINING THE VALUE OF A STOCK

Valuing stocks may be simple when using the P/E ratio and PEG ratio, or it can be more difficult when utilizing the DDM approach. Traders may determine whether there is a significant gap between a share’s market price and its intrinsic or relative value by comparing them after choosing an appropriate approach.

If there is a discrepancy between the two numbers, traders may choose to short overvalued stocks or buy long oversold stocks, but they should always use intelligent risk management.