The spectre of rising corporate debt defaults exacerbating a global economic slowdown has, for months, been largely brushed aside by resilient credit markets. However, the long-feared corporate debt woes are now starting to hit home, as more companies face downgrades to a junk credit rating, resulting in higher borrowing costs. This troubling trend is raising concerns about the stability of the global economy and the potential ripple effects on financial markets.

Concerns Mount as Companies Face Downgrades and Escalating Borrowing Costs Following the Disturbing Rise in Corporate Debt Defaults

One notable example is the retail giant Casino, burdened with a staggering €6.4 billion ($7.19 billion) net debt, which is currently engaged in court-backed talks with creditors. Similarly, Thames Water, a prominent British utility company, has been in the headlines due to its massive £14 billion ($18.32 billion) debt pile. These distressing situations highlight the challenges faced by companies struggling with mounting debt obligations.

Click here to view the Live Stock Price of the Casino Guichard

The impact of increasing corporate debt defaults is not limited to individual firms; it also poses a broader threat to the global economy. Swedish landlord SBB, downgraded to junk status in May, finds itself at the epicenter of a property crash that jeopardizes Sweden’s economy. As the property market experiences turbulence, the risk of a cascading effect on other sectors intensifies, potentially amplifying the economic slowdown.

Click here to check the Live Stock Price of SBB

Ironically, despite the mounting default risks, the cost of insuring exposure to a basket of European junk-rated corporates briefly hit its lowest point in over a year. This apparent disconnect suggests that investors remain largely unperturbed by the rising threat of defaults. However, some experts warn that complacency in the market may be overshadowing the reality of the situation.

Markus Allenspach, Head of Fixed Income Research at Julius Baer, points out that global defaults in the first five months of 2023 have already matched the total defaults recorded throughout 2022. This alarming statistic raises questions about the market’s seemingly relaxed stance. Despite the surge in defaults, high-yield bonds continue to attract inflows, indicating a paradoxical situation where investors appear undeterred by the increasing risks.

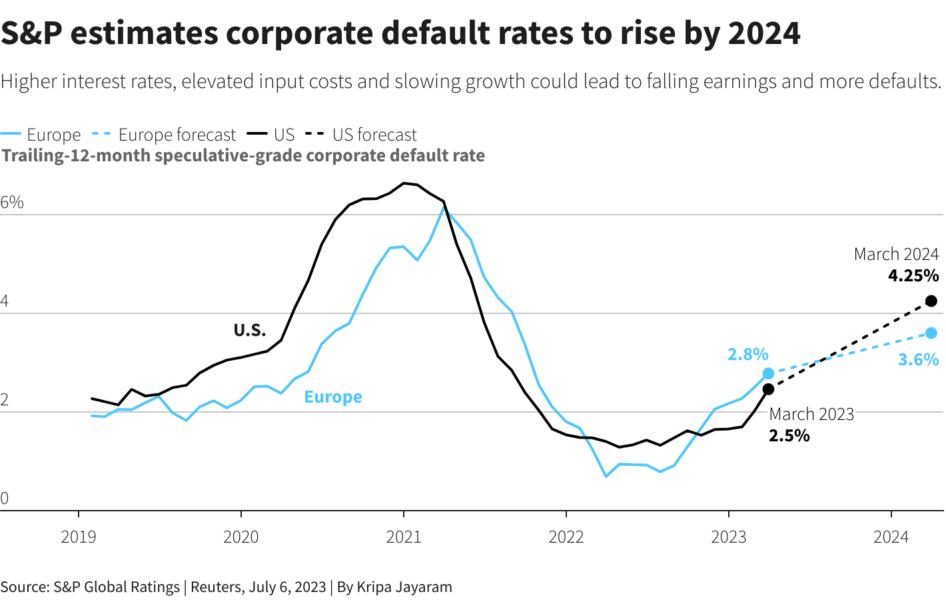

S&P Global forecasts an uptick in default rates for sub-investment grade companies in the United States and Europe. By March 2024, the default rate is expected to reach 4.25% for U.S. companies and 3.6% for European counterparts, up from 2.5% and 2.8%, respectively, in March 2023. These projections emphasize the urgent need for vigilance and caution in the face of a potentially deteriorating corporate debt landscape.

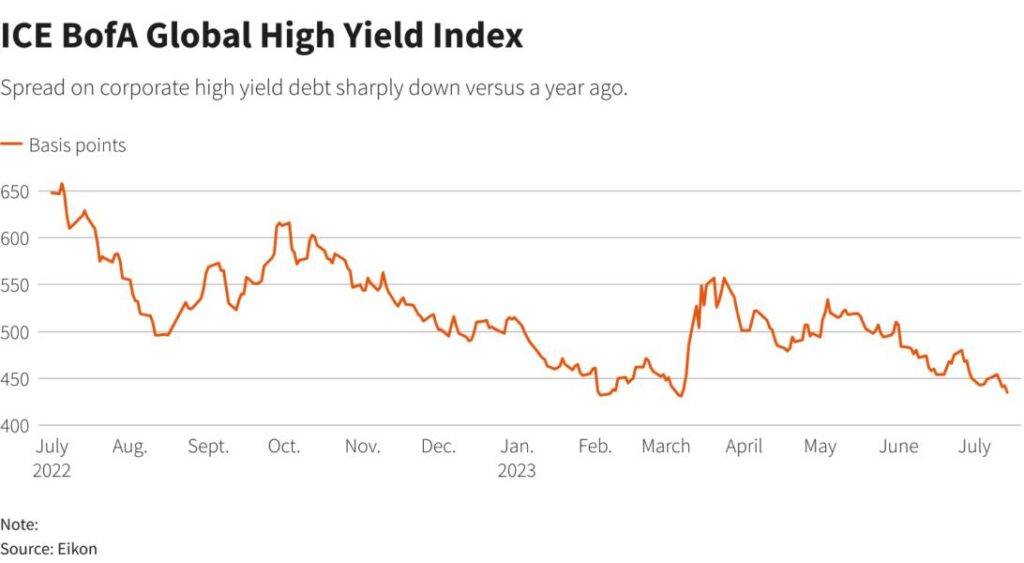

While hopes for a resilient global economy and the anticipation of an end to aggressive interest rate hikes may explain the current upbeat sentiment, analysts caution that the full impact of rate rises has yet to be fully felt. For some, this implies that corporate bond yields should command a higher premium. However, the current spread on the ICE BofA global high yield bond index stands at 435 basis points (bps), significantly lower than the 622 bps observed just a year ago. This discrepancy suggests that corporate credit spreads do not adequately reflect the underlying risks present in the market.

Guy Miller, Chief Market Strategist at Zurich Insurance Group, highlights the concerning trend of tight corporate credit spreads, which fail to mirror the existing risks. Miller points out that 122 U.S. public and private companies with liabilities exceeding $50 million have already filed for bankruptcy protection this year. At this rate, bankruptcies are projected to exceed 200 by the end of the year, comparable to levels witnessed during the global financial crisis and the COVID-19 pandemic.

The looming challenge for many firms lies in the refinancing of their debt, especially those facing imminent debt maturities. While some companies took advantage of the low interest rate environment to extend the maturity of their debt, buying themselves some time, the cost of refinancing is expected to be significantly higher for those with upcoming debt obligations.

ABN AMRO highlights a worrying trend of decreasing average maturity for European high-yield corporate bonds. In May, the average maturity reached a record low of nearly four years, compared to an average of just over six years from 2005 to 2007, a period when the European Central Bank raised interest rates. This shortened timeline leaves firms with less room to refinance their debt, resulting in more immediate and impactful effects from higher interest rates.

Faced with higher interest costs and declining profits, companies may struggle to meet their financial obligations, leading to defaults. Consequently, to avoid immediate debt repayment or insolvency, many firms are initiating talks with creditors to restructure their debt and revive their businesses. Although the legal systems and restructuring mechanisms have evolved since the financial crisis, allowing for a more predictable outcome, not all companies will be able to weather the challenges posed by vast debt burdens, higher interest rates, and increased business costs.

Conclusion

As the global economy faces an uncertain future, it is crucial to closely monitor the rising corporate debt defaults and their potential implications. Investors, businesses, and policymakers must remain proactive in identifying vulnerabilities and implementing necessary measures to mitigate risks. The road ahead may be challenging, particularly in Europe, where the downturn may be less severe but the recovery slower. Only through prudent management, cooperation, and effective risk mitigation strategies can we navigate the troubled waters of rising corporate debt and safeguard the stability of the global economy.

Click here to read our latest article on the Crude Oil Price Retreat