In today’s competitive business landscape, understanding financial metrics is crucial for success. Among these metrics, EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) stands out as a powerful tool.

This profitability metric allows businesses, investors, and analysts to measure a company’s operating performance without being influenced by financing decisions, tax strategies, or non-cash accounting items like depreciation and amortization.

By focusing on a company’s earnings from its core operations, EBITDA provides a clear picture of its potential to generate profit, making it a critical metric for determining long-term business success.

While it has become widely used, it’s essential to understand how it differs from other financial indicators. It can be calculated from either operating income or net income, each offering a slightly different perspective. Regardless of the method, EBITDA helps eliminate the noise created by financial complexities and offers a straightforward view of a company’s profitability.

In this article, we’ll explore how it works, why it’s such a valuable metric, and how it transforms the way we measure business success.

What Exactly Is EBITDA?

EBITDA is often referred to as a profitability metric that gives businesses and investors a clearer sense of operating performance. It strips away the effects of interest payments, taxes, depreciation, and amortization, focusing solely on a company’s earnings from its core operations. This makes EBITDA an invaluable tool when comparing companies within the same industry, regardless of their capital structure or tax strategies.

The formula for EBITDA is relatively simple. It can be derived from operating income or net income:

- EBITDA = Operating Income + Depreciation & Amortization

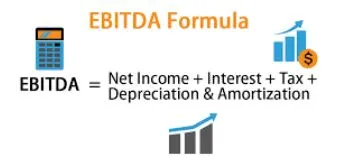

- EBITDA = Net Income + Taxes + Interest Expense + Depreciation & Amortization

By eliminating interest and tax expenses, it enables stakeholders to assess how well a company performs in its day-to-day business operations. It also excludes depreciation and amortization, which are non-cash charges that can distort the financial picture, especially for companies with significant fixed assets.

The Role of Operating Income in EBITDA

Operating income is the profit a company generates from its core business activities. It is calculated by subtracting operating expenses (such as labor costs, raw materials, and overhead) from revenue. Unlike net income, operating income does not account for interest payments or taxes. This makes it a cleaner starting point for calculating.

When you use operating income to calculate EBITDA, you are essentially looking at how much profit a company generates before accounting for financial and accounting decisions. Adding back depreciation and amortization to operating income helps you arrive at a more accurate picture of the company’s performance, as these expenses are non-cash items that do not affect cash flow.

Example:

- Operating Income: $10 million

- Depreciation & Amortization: $2 million

- EBITDA: $12 million

For example, imagine a company that manufactures heavy machinery. The company invests heavily in fixed assets, and over time, the depreciation on these assets reduces the reported income. However, by focusing on EBITDA, you can see beyond these depreciation charges and get a better sense of the company’s operational profitability.

Net Income and Its Impact on EBITDA

While operating income offers a clean view of profitability, net income represents a company’s total earnings, accounting for everything from operating activities to interest expenses, taxes, and even one-time charges. Using net income to calculate EBITDA can sometimes give a different result because it includes all these additional factors.

To calculate this using net income, we add back interest expense, taxes, depreciation, and amortization. This gives a better view of how the company is performing operationally, excluding the effects of external financial decisions.

Example of EBITDA using Net Income:

- Net Income: $5 million

- Interest Expense: $1 million

- Taxes: $2 million

- Depreciation & Amortization: $3 million

- EBITDA: $11 million

Let’s consider a retail company that recently underwent a major restructuring. If you only look at net income, you may be misled by one-time charges related to the restructuring. By focusing on EBITDA, you get a clearer picture of the company’s profitability from its regular business activities, excluding any anomalies caused by extraordinary events.

EBITDA as a Profitability Metric for Business Evaluation

EBITDA serves as one of the most commonly used profitability metrics for evaluating businesses. By excluding interest, taxes, depreciation, and amortization, EBITDA offers an apples-to-apples comparison between companies, regardless of their size, industry, or financial strategies.

Investors and analysts often turn to EBITDA to gauge a company’s ability to generate earnings from its core operations. This is particularly useful when comparing companies in industries with heavy capital investment and fixed assets, such as manufacturing or energy. In these sectors, depreciation and amortization can skew profitability measures like net income, making it a more reliable metric for comparing companies on equal footing.

Benefits of EBITDA in Profitability Evaluation:

- Capital Structure Agnostic: EBITDA removes the influence of interest payments, making it easier to compare companies with different financing structures.

- Operational Focus: By excluding taxes and depreciation, EBITDA highlights a company’s ability to generate earnings from core business activities.

- Cross-Industry Comparisons: It enables comparisons between companies in various industries, from tech to manufacturing, by stripping away differences in accounting practices.

Consider a company in the oil industry, which owns large oil rigs and machinery. These assets lose value over time due to wear and tear, leading to significant depreciation charges. If you calculate profitability based on net income, these depreciation expenses might make the company appear less profitable than it really is. However, by using this, you get a better sense of its core operational performance without the distortion of depreciation.

The Advantages of Using EBITDA

EBITDA’s primary advantage is that it simplifies financial analysis by focusing on a company’s core operations. Here are some key benefits:

- Clearer comparison across companies: Since EBITDA excludes interest, taxes, depreciation, and amortization, it provides a consistent way to compare companies, even if they operate in different tax jurisdictions or have varying financing structures.

- Focus on operational profitability: By eliminating non-cash items and financial costs, EBITDA provides a cleaner view of a company’s ability to generate profit from its day-to-day activities.

- Cash flow indicator: Although it isn’t a direct measure of cash flow, it can act as a rough proxy. By removing non-cash charges like depreciation, it gives an idea of the cash that the company is generating from operations.

- Capital structure neutrality: EBITDA does not account for how a company is financed (equity vs. debt), making it a more objective measure of operational performance.

The Limitations of EBITDA

Despite its many advantages, it does have its limitations. Since it excludes depreciation and amortization, it can sometimes overestimate the profitability of companies with large investments in fixed assets. Additionally, this doesn’t account for changes in working capital or capital expenditures, which are crucial for understanding a company’s ability to sustain and grow its operations.

For instance, a technology startup with minimal assets but high revenue might show a strong EBITDA figure. However, if the company needs to invest heavily in research and development (R&D) or marketing to sustain growth, it alone might not paint the full picture of its financial health.

Limitations of EBITDA:

- Overestimation of profitability: Companies with significant fixed assets may appear more profitable due to the exclusion of depreciation.

- Lack of capital expenditure consideration: EBITDA ignores necessary investments in future growth, such as R&D or infrastructure.

- Not a complete cash flow measure: Although it provides insight into earnings, EBITDA does not account for all cash inflows and outflows.

How to Use It in Valuation and Investment Decisions?

One of the most common methods for valuing a company is the enterprise value (EV) to EBITDA ratio. This multiple compares a company’s total value (including debt) to its EBITDA, providing insights into whether the company is overvalued or undervalued relative to its earnings potential.

Example of EV/EBITDA Ratio:

- Enterprise Value (EV): $100 million

- EBITDA: $20 million

- EV/EBITDA Ratio: 5x (This indicates that investors are valuing the company at 5 times its annual EBITDA)

For example, if a company has an EV/EBITDA ratio of 8x, it means the market is valuing the company at eight times its annual EBITDA. A higher multiple might indicate that investors have high expectations for the company’s future growth, while a lower multiple could suggest the market is undervaluing the company.

When making investment decisions, analysts often use it to determine whether a stock is priced appropriately. They will compare a company’s EBITDA margin (EBITDA as a percentage of revenue) to industry averages or to other companies in the same sector. A high margin might indicate that a company is efficiently managing its operations and costs, while a low margin could suggest that the company is struggling with profitability.

Example

Let’s take the case of a well-established company in the automotive sector. Suppose the company has been in business for several decades, owns significant manufacturing assets, and generates high revenue. However, its income statement shows relatively low net income due to large depreciation expenses on its fixed assets, such as factories and machinery.

For an investor trying to understand the company’s true profitability, EBITDA is the key metric. By calculating this, they can see the company’s operational earnings without the impact of depreciation. This allows them to make a more informed decision, especially when comparing the company’s profitability to that of competitors with different asset structures.

Conclusion

EBITDA is undeniably one of the most important profitability metrics in the business world today. By focusing on earnings from core operations and excluding non-cash items like depreciation and amortization, EBITDA provides a clear and objective view of a company’s financial performance. It serves as a valuable tool for investors, analysts, and business owners alike, offering insights into profitability, cash flow potential, and long-term success.

While it’s not without its limitations, when used correctly, it transforms the way businesses measure their financial health and helps investors make more informed decisions. Whether evaluating operational efficiency, comparing companies, or determining company valuations, EBITDA is an essential metric that cannot be overlooked.

Click here to read our latest article Forex Trading: Where Strategy Beats Luck