Price inflation in an economy is influenced by money supply growth and changes in productivity and resource abundance. Fast bank lending and fiscal deficits, along with the impact of high interest rates, can create inflation, while austerity and private sector deleveraging lead to disinflation or deflation. Factors like technological stagnation, societal dysfunction, and scarce resources contribute to inflation, while technological advancements and abundant resources contribute to disinflation.

For example, the price of oil in gold and dollars fluctuates based on supply and demand, with the dollar showing an exponential trend due to currency debasement. Central banks, with the ability to influence credit creation, impose rules on banking systems, and print money to finance deficits, play a significant role in managing inflation, including through the utilization of high interest rates, especially during crises when their independence may diminish.

This article explores the impact of interest rate adjustments on money creation and price inflation, considering the context in which they are implemented.

Sources of Money Creation

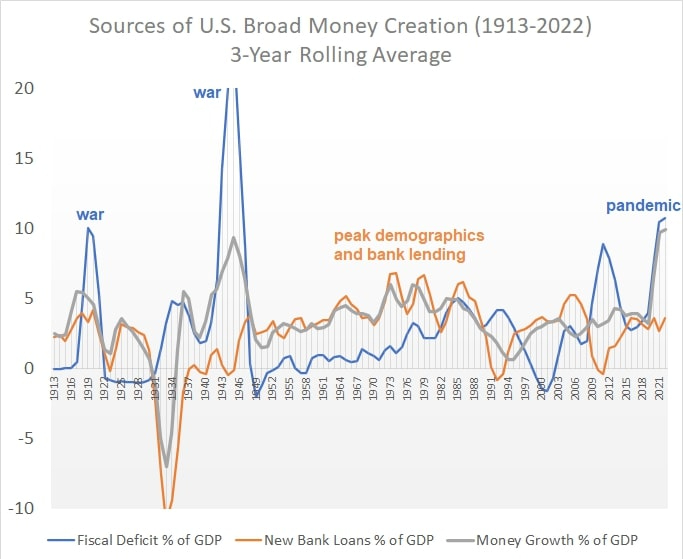

Money creation in the current financial system is primarily driven by fiscal deficits and bank lending, with their relative importance changing over time. In periods like the 1940s and 2020s, fiscal deficits fueled most of the money supply growth, while bank lending played a larger role in the 1970s. It’s crucial to understand these distinct causes of inflation to effectively address it. Visual representations, such as charts illustrating the U.S. fiscal deficits, new bank loans, and broad money supply growth over time, provide valuable insights.

However, it’s recommended to familiarize oneself with the mechanisms behind fiscal deficits and bank lending in creating broad money for a better understanding. Currently, Fed Chairman Jerome Powell is responding to the 2020s inflation, driven by fiscal deficits in a high public debt environment, as if it were similar to the lending-driven inflation of the 1970s with low public debt. This approach involves raising interest rates to curb bank lending, despite it not being the primary cause of inflation in this cycle, leading to potentially unexpected outcomes depending on various factors.

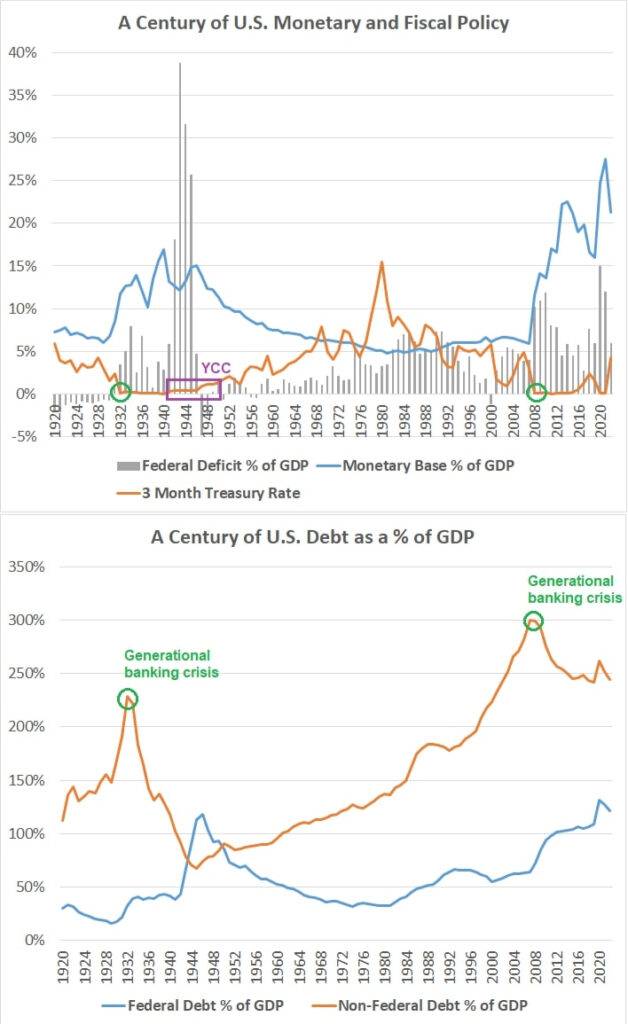

This chart shows the overall history of U.S. fiscal and monetary policy since 1920:

The Relationship between Interest Rates and Inflation

The impact of interest rates on money creation and inflation is often misunderstood. While some believe that high interest rates are both necessary and sufficient to combat price inflation, historical data shows that this is not always the case. Interest rates are just one tool among many in a central bank’s arsenal and their influence on inflation is indirect and context-dependent.

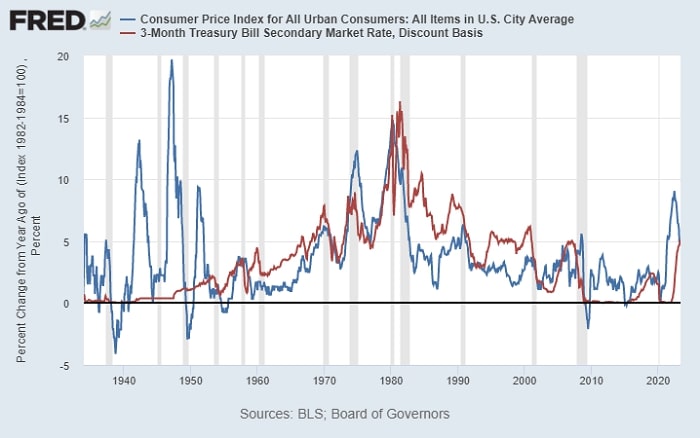

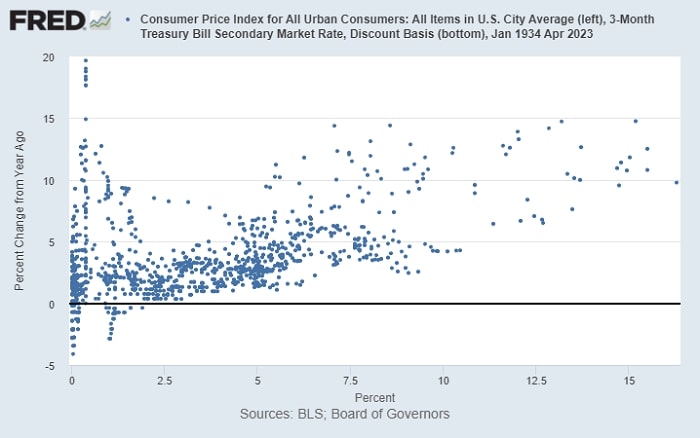

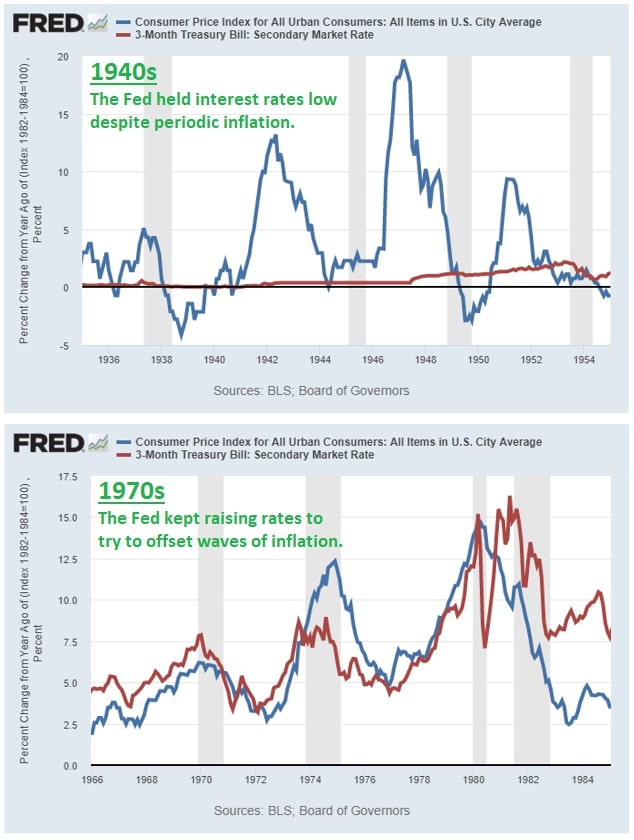

Looking at the correlation between short-term interest rates and official consumer price inflation since 1934, there appears to be a weak relationship. Central bankers typically raise interest rates in response to high inflation, but there are periods where there is no correlation, such as in the 1940s. This is because inflation is influenced by multiple variables, and interest rates play a specific role.

Stanley Druckenmiller once stated that inflation never comes down unless the Fed Funds rate surpasses the Consumer Price Index (CPI) when inflation exceeds 5%. While Druckenmiller is an esteemed macroeconomic trader, he is factually incorrect in this case. In the 1940s, inflation returned to normal levels even when interest rates were kept below the inflation rate. This was due to the unique circumstances of inflation during that period, which was primarily driven by monetized fiscal spending on the war. When the war ended and fiscal deficit spending ceased, inflation subsided.

When inflation is caused by runaway fiscal deficits, raising interest rates does not effectively address the issue. In such cases, the central bank and the banking system are compelled to finance the government’s deficits, and changes in interest rates have limited impact compared to the primary cause of inflation. Raising interest rates may temporarily slow inflation by reducing bank lending and dampening the overall economy, but it does not tackle the root cause directly.

Over time, persistently high interest rates in an inflationary environment driven by fiscal deficits can exacerbate inflation. Higher interest rates on public debt lead to larger deficits as interest payments increase, injecting more money into the economy. Unlike households or corporations that can default on debt, a sovereign government can continue to print money through its central bank to cover the deficit, resulting in increased money supply. Thus, raising interest rates sharply during the war in the 1940s would likely not have curbed inflation, but rather worsened it.

On the other hand, if interest rates are at or below the inflation rate, it creates an incentive for borrowing and investment in hard assets. Bank lending increases the money supply, contributing to a vicious cycle of inflation. For example, if inflation is 5% per year and a mortgage can be obtained at a 3% interest rate, borrowing becomes attractive, especially when acquiring hard assets. As banks issue mortgages, they create more money in the system through the fractional-reserve banking system. This leads to higher asset prices and money supply growth, intensifying inflationary pressures.

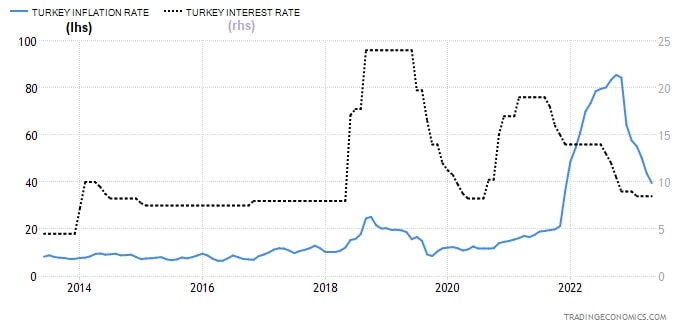

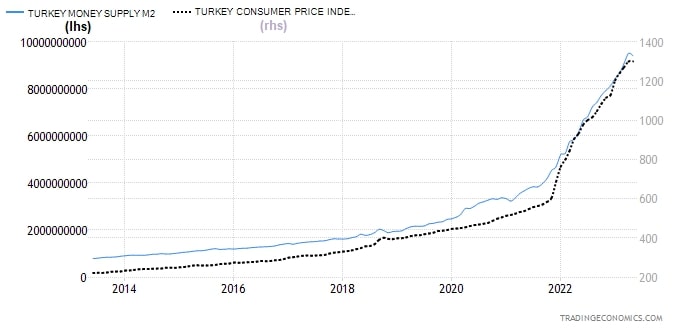

A notable example is Turkey, where inflation skyrocketed while interest rates ranged between 8% and 18%. The market incentive to borrow Turkish lira and invest in more stable assets drove inflation higher. The country experienced a surge in money supply and inflation due to borrowing and a lack of confidence in the currency.

It’s important to understand that the relationship between interest rates and inflation is complex and multifaceted. Debates often arise among analysts, focusing on either the bank lending channel or the fiscal deficit channel of money creation, without considering both simultaneously. Additionally, this topic tends to be politicized, leading to conflicting viewpoints and misunderstandings.

Simply advocating for higher interest rates as a solution to inflation overlooks the fact that fiscal deficits are the primary driver of inflation in the current cycle, akin to the 1940s. Conversely, maintaining low interest rates, as attempted by Turkey, can exacerbate inflation caused by bank lending and speculative attacks on the currency.

Navigating the Complexities of Inflation

Understanding and addressing inflation is a complex task. By examining historical examples and current economic conditions, we can better assess the measures necessary to combat inflation within the existing financial system. It becomes evident that certain combinations of factors make it exceptionally challenging for central banks to address inflation effectively.

The Role of Money Supply Growth and Supply of Goods and Services

To curb aggregate price inflation, it is crucial to maintain low money supply growth relative to the growth in the supply of goods and services. While this principle sounds simple, implementing it in practice can be challenging, particularly in specific economic scenarios. Evaluating these factors helps determine the effectiveness of measures taken to combat inflation and their structural impact.

Different Scenarios and Historical Examples

Inflation caused by war or a demographics bulge accompanied by high bank lending can be fixed. War-driven inflation diminishes after the war ends, and fiscal conditions return to normal. Similarly, lending-driven inflation can be controlled by natural demographic shifts or by tightening monetary policy. Historical examples, such as the United States in the 1910s, 1940s, and 1970s, illustrate different approaches to addressing inflation based on prevailing conditions and debt-to-GDP ratios.

The Toughest Inflation Combination

The most challenging scenario for central banks is when there is a high sovereign debt-to-GDP ratio, large fiscal deficits linked to aged demographics and imbalanced entitlement programs, high military spending, and significant supply constraints. This situation differs from the 1970s as it poses a greater threat due to high public debt levels. Following the 1940s playbook, which involves keeping interest rates low despite high inflation, may reduce fiscal-driven inflation but could lead to speculative attacks on the currency. On the other hand, adopting the 1970s playbook and significantly raising interest rates could temporarily reduce money creation from bank lending but exacerbate inflation in the long term by widening fiscal deficits.

The Dilemma and Potential Solutions

The challenging environment described above presents policymakers with a difficult choice between fiscal-driven inflation and lending-driven inflation. Various restrictions, such as capital controls, may be implemented to limit borrowing and speculative attacks on the currency. However, capital controls can result in a command-and-control economy and create incentives for capital flight. The government may use these restrictions as a means of reprogramming the test, attempting to reduce interest rates to combat fiscal-driven inflation while also preventing a weakening currency.

Addressing inflation in complex economic environments requires a multifaceted approach. Balancing interest rates, fiscal deficits, and supply constraints is crucial but challenging. Political dynamics can further complicate matters, as different viewpoints emerge on the appropriate level of interest rates and government spending. To address the underlying causes of inflation, structural adjustments to public debt, taxation, spending, and promoting industrial and energy production may be necessary. Achieving a foundation for long-term disinflationary growth amidst such complexities is difficult but essential for sustained economic stability.

Conclusion

High interest rates can help slow down bank lending and encourage entities to hold the currency, reducing money supply growth from borrowing and speculative attacks on the currency. However, high interest rates can also worsen deficit-driven inflation, particularly when countries have high sovereign debts and deficits. Each increase in interest rates puts pressure on the private sector, but it also leads to larger public sector deficits that pour money into the economy.

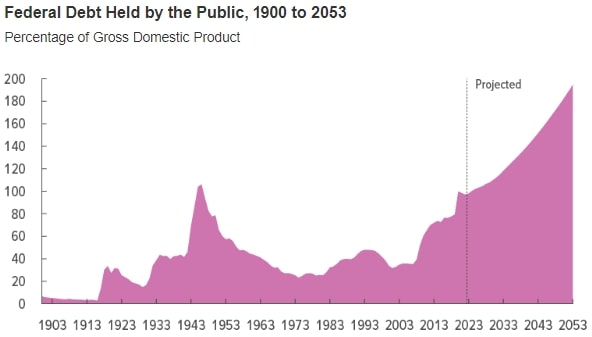

Many developed countries, including the United States, currently have high debt-to-GDP ratios and large deficits, making low interest rates necessary to prevent further fiscal-driven money creation over several years. However, in an inflationary resource-constrained situation, low interest rates may encourage excess bank lending, leading to an acceleration of money creation, or result in higher import and energy prices.

To navigate this situation, governments attempt to restrain bank lending while maintaining workable interest rate expenses and liquidity. The politicization of interest rates arises from these challenges. The impact of recent interest rate increases has not fully affected the private or public sector yet, as there is a long and variable lag.

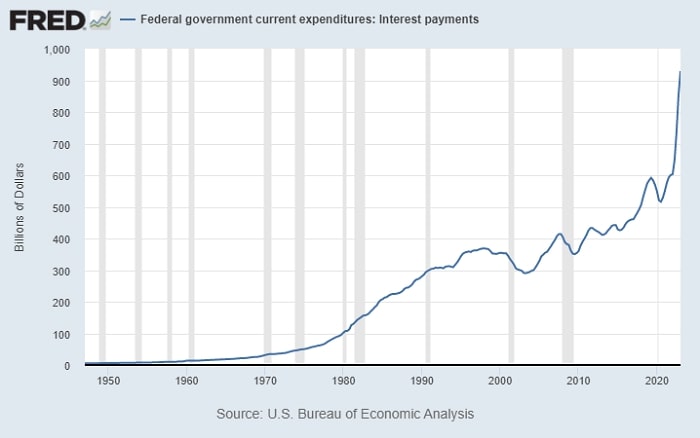

For the private sector, as more private debt matures and gets refinanced at higher rates, it will act as a disinflationary and recessionary force, particularly affecting interest rate-sensitive sectors. In contrast, for the public sector, the refinancing of longer-term federal debt at higher rates serves as an inflationary and stimulatory force. With $32 trillion in debt, sustained 4-6% interest rates would result in annual interest expenses of $1.3 to $1.9 trillion, adding to the deficit and pouring into the economy.

Thus, stagflationary conditions persist with conflicting forces. Currently, the cyclical disinflationary side is gradually gaining momentum after a period of rapid fiscal money creation, but high inflation is likely to return during the decade, especially during the next economic acceleration.

Click here to read our article on Mastering Breakout Trading