Quantitative tightening (QT) is a contractionary monetary policy instrument that central banks employ to lower an economy’s level of liquidity, money supply, and overall economic activity.

You may be wondering why a central bank would want to slow down economic activity. When the local economy overheats and inflation, or the overall rise in the cost of goods and services commonly bought there, occurs, they reluctantly do so.

The Benefits and Drawbacks of Inflation

Because a steady rise in the overall level of prices is essential to healthy economic development, most industrialized countries and their central banks have a modest inflation goal of approximately 2%. The essential concept here is “steady,” which makes forecasting and long-term financial planning for both people and organizations simpler.

The Wage-Price Spiral and Inflation

However, when employees agitate for higher pay owing to greater inflation expectations, a cost that firms pass on to consumers through higher prices, which decreases consumers’ buying power, eventually leads to more wage adjustments, and so on, runaway inflation may quickly get out of hand.

Quantitative easing (QE), a contemporary monetary policy tool that involves sizable asset purchases (typically a combination of government bonds, corporate bonds, and even equity purchases) used to stimulate the economy in an effort to recover from a severe recession, carries a very real risk of inducing inflation. Overstimulation may cause inflation, which may need quantitative tightening to undo the negative impacts of QE (surging inflation).

QUANTITATIVE TIGHTENING: HOW DOES IT WORK?

By selling its acquired assets, mostly bonds, a central bank may tighten up the money supply in the economy. This process is known as quantitative tightening. The process by which the central bank shrinks its bloated balance sheet is known as “balance sheet normalization” as well.

Quantitative Tightening’s Objectives:

- Reduce the quantity of currency in use (deflationary)

- Increase borrowing costs in tandem with an increase in the benchmark interest rate

- Reduce the economy’s temperature without causing the financial markets to become unstable

Bond sales in the secondary treasury market are one way to implement QT, and if there is a large increase in the supply of bonds, the yield or interest rate needed to attract purchasers will often increase. The hunger of businesses and people who previously borrowed money while lending circumstances were hospitable and interest rates were close to (or at) zero is reduced by higher yields, which also increase borrowing costs. Less borrowing causes consumers to spend less, which, in turn, reduces economic activity and, in principle, cools asset values. Additionally, the act of selling bonds depletes the financial system’s liquidity, prompting individuals and firms to exercise greater restraint when making purchases.

TAPERING VS. QUANTITATIVE TIGHTENING

The word “tapering,” which is often used to refer to the quantitative tightening process, really refers to the time between the quantitative easing and the quantitative tightening, when large-scale asset purchases are reduced in size before being stopped entirely. The revenues from ageing bonds are often reinvested in fresh bonds under QE, so injecting additional money into the economy. However, tapering is the process through which reinvestments are reduced until they finally stop.

The word “tapering” is used to characterize the smaller incremental extra asset acquisitions, which are just slowing down the pace at which central banks are acquiring assets rather than “tightening.” For instance, even though the automobile will begin to slow down, presuming you are on a level road, you wouldn’t refer to pulling your foot off the gas pedal as breaking.

QUANTITATIVE TIGHTENING EXAMPLES

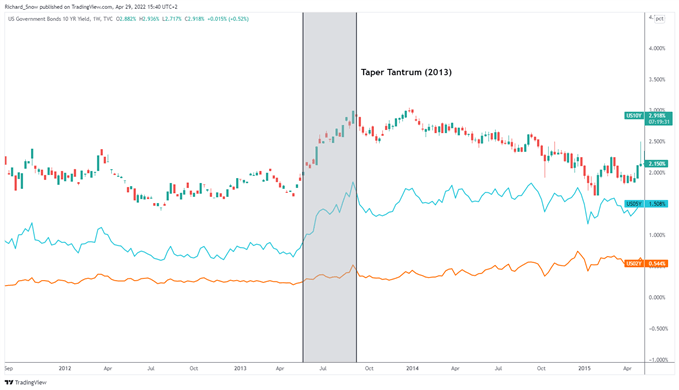

Since QE and QT are relatively recent policy instruments, there haven’t been many opportunities to investigate QT. The Bank of Japan (BoJ) was the first central bank to use QE, but owing to persistently low inflation, it has never been allowed to use QT. The US deployed QT once only for it to be abruptly cancelled less than a year later in 2019 due to poor market circumstances. QT was delayed until 2018, as previously mentioned, in 2013 when Fed Chairman Ben Bernanke’s mere suggestion of tapering threw the bond market into a tailspin. Due to the brief duration of the programme, the technique has not been fully evaluated.

The Federal Reserve has $9 trillion on its balance sheet as of 2008, and between 2018 and 2019, the amount barely marginally decreased. There has only been one way traffic since then.

The Fed’s assets have grown throughout time (peaking slightly about $9 trillion).

QUANTITATIVE TIGHTENING’S POSSIBLE DRAWBACKS

A precise balance must be struck while implementing QT in order to remove money from the system without causing financial markets to become unstable. The prospect of central banks withdrawing liquidity too soon might frighten financial markets and cause unpredictable fluctuations in the bond or stock market. This is precisely what occurred in 2013, when Federal Reserve Chairman Ben Bernanke just suggested that asset purchases may be curtailed in the future, leading to a sharp increase in Treasury rates and a subsequent decline in bond prices.

Weekly Chart of US Treasury Yields (orange 2yr, blue 5yr and 10 year yields)

Such an occurrence is known as a “taper tantrum,” and it may still occur throughout the QT interval. The fact that QT has never been completed is another disadvantage. After the Global Financial Crisis, QE was put into place in an effort to lessen the severe economic crisis that followed. After Bernanke’s remarks, the Fed opted against tightening and instead chose to execute a third round of QE until more recently, in 2018, when the Fed started the QT process. Due to the unfavorable market circumstances, the Fed chose to discontinue QT less than a year later. Since there is no other precedent, it is possible that future QT installation may once again have a detrimental impact on the market.