Talking points include the S&P 500, FED, Boston, China, Crude Oil, OPEC+, US Dollar, Gold, and NZD.

- Going into Friday’s session, the S&P 500 has had a respite.

- Chinese lockdowns and Fed tightening are lowering economic expectations.

- All eyes will be on today’s US non-farm payrolls. The S&P 500 will it rise?

The S&P 500 originally tested lower before ending the cash session up 0.30%. Futures indicate that trade will begin slowly today. The aggressive stance of the Federal Reserve and China’s meagre economic prospects seem to be obstructing the prognosis for global growth.

Raphael Bostic, president of the Atlanta Federal Reserve, added to his overnight hawkish commentary by stating that “when you push demand down, it carries the potential of slowing the economy down.” Additionally, he used the R-word. The yield on 2-year Treasury bonds is still close to a 15-year high.

As long as the zero-case Covid-19 policy is in effect, the Chinese city of Chengdu has been placed under lockdown. There are power outages and drought conditions in the Sichuan district’s 21 million-person metropolis.

Industrial metal prices have significantly decreased as a result of the dim outlook for Chinese economic development and growing concern worldwide about tighter monetary policy slowing down the global economy.

Hong Kong’s Hang Seng index and China’s CSI 300 index are both down. The Nikkei 225 in Japan is down on the day as well, although the ASX 200 in Australia is marginally up.

In anticipation of the Organization of Petroleum Exporting Countries (OPEC+) meeting next week, crude oil futures prices rose Wednesday. To counteract pressure on the price of the energy source, the cartel is contemplating reducing output. While the Brent contract is close to US$ 94 barrel, WTI is over US$ 88 bbl.

After losing ground into the North American close, gold has been stable so far today, trading around US$ 1,700.

Except for the Kiwi Dollar, the foreign exchange market has been rather calm as of Friday. The declining terms of trade numbers have further weakened the currency that is tied to growth. Overall, the US dollar is still trading close to record highs.

The market will be eagerly watching today’s US non-farm payroll figures. After then, data on durable products and manufacturing orders will be made available.

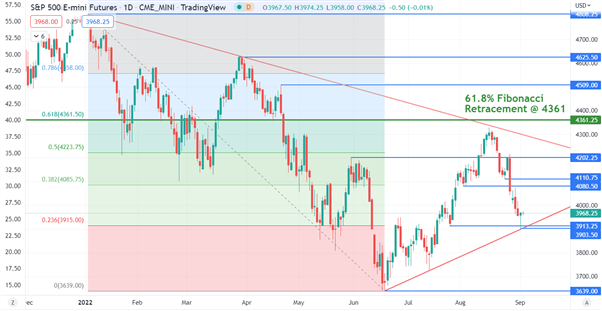

Technical analysis of the S&P 500

The 61.8% Fibonacci Retracement and a declining trend line, both around 4361, prevented the S&P 500 from breaking above them last month.

Since then, it has fallen, and yesterday, it made a low of $3903 after rebounding off an upward trend line. Support might come from that trend line as well as the two preceding lows in the 3903–3913 region.

The break points at 4080, 4110, and 4202 may provide resistance on the topside.