The US dollar, as measured by the DXY index, is facing downward pressure as traders eagerly await the crucial Federal Open Market Committee (FOMC) decision. Market participants are closely monitoring the levels on the DXY index, anticipating potential shifts in the currency’s value. The May US inflation data has added to the uncertainty, increasing the likelihood of a Fed pause in the June meeting. However, the overall tightening cycle may not yet be over.

Market anticipation builds as traders assess US Dollar’s fate amid upcoming FOMC announcement

Policymakers’ guidance and macroeconomic projections will play a significant role in determining the trading bias of the US dollar in the coming days and weeks. Traders are particularly interested in the dot plot, which will provide insights into the expected extent of additional tightening and whether policymakers are considering a more accommodative approach in the future.

Amidst this environment of cautious market sentiment, the US dollar, as measured by the DXY index, weakened on Tuesday. However, it’s important to note that the initial reaction to the morning’s US economic data, which indicated a cooling of annual headline inflation to 4.0% in May, weighed on the currency temporarily. Traders swiftly reassessed the situation, realizing that the Federal Reserve could potentially resume rate hikes in July and maintain higher rates for a longer duration.

Tomorrow’s June decision by the US central bank, along with the updated summary of economic projections, will provide further clarity on the monetary policy outlook. Traders will be closely observing any indications of additional rate rises and whether policymakers intend to adopt a more relaxed stance in 2023. The dot plot, in particular, could reveal the possibility of one or even two more 25 basis-point hikes for 2023, with the potential absence of rate cuts through 2024. Should this hawkish scenario materialize, short-dated nominal yields are likely to rise, driving the US dollar higher in the near term.

Conversely, if the Federal Reserve refrains from signaling further rate increases compared to its previous estimates and keeps the door open for a less restrictive stance in 2023, the outcome becomes uncertain. Such a scenario could have bearish implications for both yields and the US dollar.

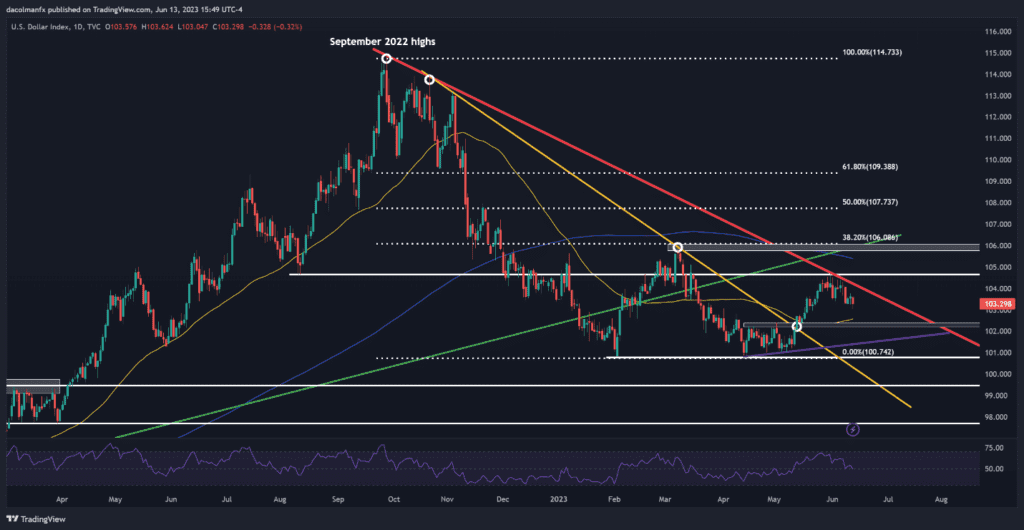

From a technical analysis perspective, the US dollar index has been on a downward trajectory since the beginning of the month, unable to break above the medium-term trendline resistance that has been in play since September of last year. In the days and weeks ahead, if the decline gains momentum, initial support can be found in the range of 102.40 to 102.15. Further weakness would shift attention towards 101.50.

Source dailyfx

On the other hand, if buyers regain control and initiate a bullish turnaround, the first notable resistance lies at the psychological level of 104.00, which coincides with trendline resistance. A decisive breakthrough above this barrier could potentially lead to a move towards 104.70, followed by a potential retest of the 200-day simple moving average.

As the countdown to the FOMC decision continues, market participants remain on edge, evaluating the US dollar’s trajectory and potential implications. The outcome of the Fed’s decision will undoubtedly shape the near-term direction of the US dollar, with traders carefully assessing the levels on the DXY index for signals of the currency’s future path.

The recent US economic data release, showing a cooling of annual headline inflation to 4.0% in May, has sparked speculation about the Federal Reserve’s next moves. This development has fueled expectations of a potential pause in the rate hikes during the June FOMC meeting. Traders have reacted by adjusting their positions and pricing in a temporary respite in the tightening cycle.

However, uncertainties linger as to whether this pause in rate hikes signifies the end of the tightening cycle or merely a brief intermission. Traders will be closely monitoring the upcoming FOMC decision, looking for clues in policymakers’ guidance and macroeconomic projections. The dot plot, in particular, will be scrutinized to gauge the Fed’s outlook on future rate adjustments.

Click here to check the USD Index

Conclusion

The US dollar’s performance on Tuesday reflected the initial reaction to the morning’s economic data. As news of the cooling inflation broke, the currency experienced a temporary setback. Nevertheless, market sentiment quickly shifted as traders assessed the possibility of a July rate hike and prolonged higher interest rates.

The focus now turns to the upcoming FOMC decision and its accompanying economic projections. Traders will eagerly await insights into the central bank’s stance on monetary policy. Should the dot plot reveal expectations of one or two more 25 basis-point hikes in 2023, with no rate cuts projected until 2024, the US dollar could receive a boost in the short term. This hawkish scenario is likely to result in higher short-dated nominal yields, reinforcing the currency’s strength.

However, if the Federal Reserve chooses not to revise its rate hike projections compared to March estimates and maintains a more accommodative stance for 2023, market expectations could shift. In such a scenario, both yields and the US dollar may experience downward pressure.

On the technical analysis front, the US dollar index has encountered resistance since the start of the month, failing to breach the medium-term trendline that has persisted since September of the previous year. With further decline, the initial support levels lie between 102.40 and 102.15. A sustained weakening could redirect attention to the 101.50 level.