In recent financial cycles, the phrase US Dollar Dip Pauses has consistently captured the attention of global economists, investors, and policymakers. The strength and trajectory of the US Dollar (USD) often serves as a foundation upon which many global financial strategies are built, given its undebated hegemony in the world’s economic sphere. This makes it crucial to deeply comprehend the current hiatus in the USD’s recent fall, particularly as its effects echo across different continents.

Markets on Edge: As the US Dollar Dip Pauses, Could a Sluggish Economic Landscape Be the Underlying Catalyst?

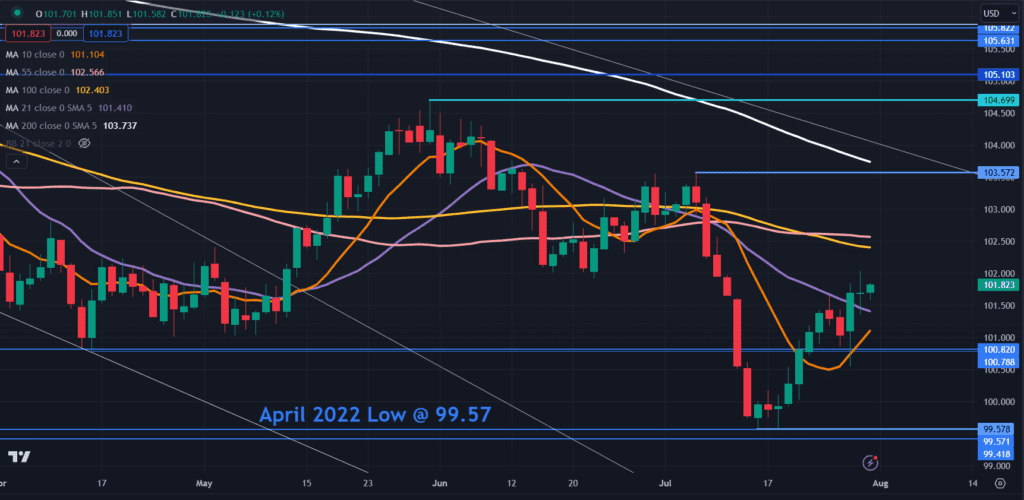

At the epicenter of this narrative is the DXY Index, which most experts view as a comprehensive reflection of the US Dollar’s strength in global markets. The past several days have seen this index stabilizing, a striking contrast to its preceding trend that witnessed three back-to-back days of depreciations. The sudden change in direction, especially after the dollar’s swift descent beneath an established ascending trendline, has left many market watchers contemplating the underlying factors and their long-term implications. At the forefront of this analysis are the Fibonacci Retracement levels, with specific emphasis on the 102.58 mark, which is representative of a 38.2% retracement.

So, what’s driving this abrupt halt in the USD’s slide? A mosaic of interrelated developments offers some clues.

One of the significant pieces in this puzzle is the future actions of the Federal Reserve, the US’s central banking system. Emerging economic indicators paint a less than rosy picture for the immediate future of the US economy. For instance, recently released figures show a downward revision of the annualized GDP for the second quarter, moving from an initial 2.4% to a slightly more conservative 2.1%. Simultaneously, the ADP employment statistics didn’t meet the market’s optimistic expectations, revealing that only 177k jobs were added in August, a noticeable drop from the projected 195k.

This array of economic revelations has triggered widespread discussions. The dominant belief is that the Federal Reserve may reconsider its previously assumed assertive stance, possibly leaning towards a more cautious monetary policy. As a testament to this evolving sentiment, Wall Street saw a notable shift in mood. Specifically, the NASDAQ index experienced a surge, registering a 0.54% rise, a phenomenon widely attributed to the market’s optimism towards a gentler Fed approach being beneficial for the equities sector.

Amidst these domestic fluctuations, the international financial arena has had its fair share of events. The exchange rate dynamics of USD/JPY, an essential metric of the symbiotic relationship between the world’s first and third-largest economies, provided an intriguing subplot. Following the release of less-than-expected Japanese industrial production data, the pair saw a brief dive to the 145.75 mark, though it managed a subsequent rebound to surpass the 146 threshold.

Shifting our gaze to the East, China has consistently been a focal point of global economic discussions. Recent developments in its beleaguered property sector have further intensified global interest. For instance, the revelation from Country Garden, a dominant force in China’s real estate domain, about its looming debt challenges, especially in light of a staggering US$ 7 billion loss in the year’s first half, has sent shockwaves across financial corridors.

Source: DFX

While these concerns remain at the forefront, it’s essential to note that not all Chinese economic data has been grim. The country’s PMI figures for the recent month pleasantly surprised many, registering a slightly upbeat 49.7 against the anticipated 49.2. Yet, these numbers, though positive, were overshadowed by the continuing anxieties surrounding China’s property and real estate sectors, casting a mixed aura over the APAC stock markets.

Europe, a significant player in this intricate financial web, is also bracing for pivotal data releases. The much-anticipated Euro-wide CPI data promises to shed further light on the continent’s economic health, which could, in turn, influence USD dynamics.

Conclusion

Understanding the recent pause in the US Dollar’s decline demands a holistic approach. It’s an intricate tapestry woven with fresh economic data, speculative strategies from central banks, and reactions from global markets. As the world waits with bated breath for subsequent developments, it’s crucial for investors and market watchers to adopt a balanced and informed approach. With the sheer unpredictability of today’s financial world, staying abreast of these intertwined narratives could be the key to making informed and lucrative decisions.

Click here to read our latest article on the Secrets of Forex Fragility