The main US stock markets have seen a sharp decrease while US Treasury rates have risen quickly. According to the conventional discounted cash flow model, increasing interest rates lower the net present value of future cash flows. Companies with heavy debt loads and little to no profitability often experience the most significant losses when interest rates rise.

A DYNAMIC MACRO ENVIRONMENT

Risk assets have found the year 2022 to be a challenging one for the most part. The Nasdaq 100, which dominates the US stock market, has dropped over -30% this year (if not more). There has been a lot of accusatory pointing. The Russian invasion of Ukraine or the Federal Reserve’s mistakes about inflation is to blame. Or the substantial financial investment made during the early months of the epidemic; or China’s zero-COVID plan, which upended the global supply chain.

The fact is that, despite the abundance of stories, from a macroeconomic standpoint, the core reason is very straightforward, though not typical: increasing interest rates. The main topic of this debate is not the increase in interest rates itself but rather how it affects traders’ and investors’ willingness to take risks in the financial markets.

FED MODEL

US equities markets have produced a better-annualized return than US Treasuries since the end of World War II. Stocks, however, also come with higher risk, and as a result, returns have been more unpredictable. The standard deviation of stock market returns has, in particular, been larger than that of bond market returns.

While stocks are riskier than bonds, their anticipated excess return makes them a potentially more tempting investment objective. The Fed Model, which contrasts the earnings yield (E/P; the opposite of the P/E ratio) of the S&P 500 with the yield on the US Treasury 10-year note, is one method for calculating this trade-off.

Investors will choose stocks over bonds as long as the earnings yield of the whole stock market is greater than the bond yield. But why would investors take on more risk in exchange for a lesser return if the S&P 500’s earnings yield falls below the US Treasury 10-year yield?

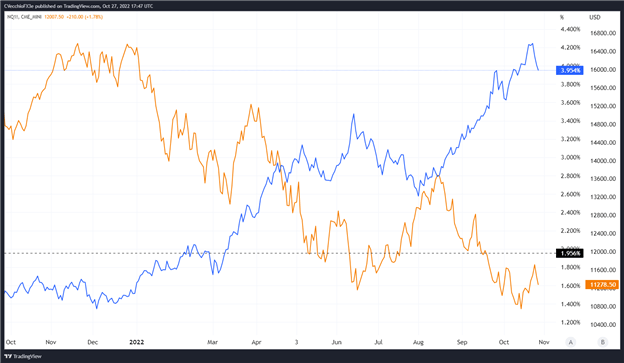

NASDAQ 100 in the United States (ETF: QQQ; FUTURES: NQ1!) Vs. TECHNICAL ANALYSIS OF THE US TREASURY’S 10-YEAR YIELD: DAILY CHART (OCT 2021 TO OCT 2022) (CHART 1)

Because bond returns are equivalent to those seen in the stock market and the increase in bond rates may be alluring enough to induce a change in asset allocation, the rise in US Treasury yields during 2022 has caused many to reassess how they are spending their capital.

FUTURE CASH FLOWS DECLINE IN VALUE

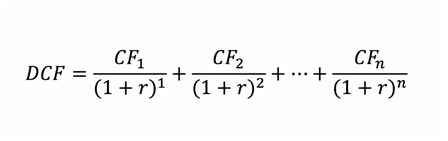

However, it is not simply the bond market’s much more alluring return profile that is to blame for the downturn in the US stock markets at a time of increasing interest rates. To get to the bottom of this, we must consult our finance 101 textbooks and the discounted cash flow (DCF) model.

The formula for Discounted Cash Flows

The net present value of all future cash flows is calculated using the DCF method by measuring the cash flows across a range of years and discounting them using the anticipated interest rate then: CF stands for cash flows, r for interest rate, and n for the time interval. The fact that r appears in the denominator indicates that the net present value of the related CF decreases as interest rates rise.

Therefore, future cash flows that a firm generates are worth substantially less today in an environment where interest rates are growing as measured by US Treasury yields. Rising interest rates imply a lower return in the future for the corporations that make up US stock markets. A company’s stock is worth less if it makes less money in the future (measured in terms of present value). And if its equity value declines, so does the value of its shares.

This link is particularly detrimental to more minor, newly established businesses with paltry cash flows and businesses that are not already cash flow positive. Newer tech firms, for example, still in the early phases of development and trying to make improvements that would transform sectors or the economy, suffer even more since they don’t have big cash flows and could be heavily indebted.

SHORT OR LONG DURATION?

By their very nature, stocks are sometimes referred to be “long duration” investments. Conceptually, duration may be explained as follows: How long would it take for me to get my $1 investment if I invest it today? Longer-term investments often suffer more when interest rates rise; since the net present value of future cash flows decreases, it will take longer for the firm to recover the $1 you invested today.

We have previously discussed the reasons behind the poor performance of Cathie Wood’s ARKK fund in the first half of 2022. The fund invests in businesses that are frequently newly founded, recently listed, lack significant established revenues and cash flows, and lack significant pricing power within their industries. In essence, ARKK is invested in the market’s longest-term assets!

The Nasdaq 100, heavily weighted in technology, and the DCF formula easily explains the general stock market’s issues: the firms don’t have large (or any) cash flows, and when interest rates increase, their net present value rapidly declines.