CONTRACTIONARY MONETARY POLICY: WHAT IS IT?

The process through which a central bank employs different measures to reduce inflation and the overall level of economic activity is known as contractionary monetary policy. A mix of interest rate increases, increased reserve requirements for commercial banks, and quantitative tightening, often known as large-scale government bond sales, are the methods used by central banks to accomplish this (QT).

It may seem counterintuitive to desire to reduce economic activity, but doing so has unintended consequences like inflation, which is the overall increase in the cost of ordinary products and services used by people when an economy is growing faster than it can maintain.

As a result, central bankers use a variety of monetary instruments to purposefully reduce economic activity without causing the economy to collapse. Officials deliberately adjust financial circumstances, causing people and companies to think more carefully about their present and future spending patterns. This delicate balancing effort is often referred to as a “soft landing.”

A period of supportive or “accommodative monetary policy” (see quantitative easing) in which central banks ease economic conditions by lowering borrowing costs by lowering the nation’s benchmark interest rate and by increasing the amount of money available in the economy through large-scale bond sales is frequently followed by a period of contractionary monetary policy. The cost of borrowing money is almost free when interest rates are close to zero, which encourages investment and general spending in an economy coming out of a recession.

Tools for contractionary monetary policy

The benchmark interest rate is increased, as are the reserve requirements for commercial banks and large-scale bond sales, by central banks. The following examines each:

1) Raising the Key Interest Rate

The interest rate that a central bank charges commercial banks for overnight loans is referred to as the benchmark or base interest rate. It serves as the basis from which other interest rates are calculated. A mortgage or personal loan, for instance, will include the benchmark interest rate plus the additional percentage that the commercial bank applies to the loan in order to generate interest income and any pertinent risk premium in order to make up for any special credit risk that an individual poses to the institution.

As a consequence, increasing the base rate also increases all other interest rates that are connected to it, increasing all interest-related expenses. Since there is less disposable income due to higher expenses, there is less spending and less money moving about the economy.

2) Increasing the Need for Reserves

In order to cover obligations in the case of unforeseen withdrawals, commercial banks are mandated to keep a portion of customer deposits with the central bank. It also serves as a tool for the central bank to manage the flow of money into the economy. The reserve requirement may be increased by the central bank to stop commercial banks from lending money to the general people when it wants to control the quantity of money moving through the financial system.

3) Open Market Activities (Mass Bond Sales)

By selling copious quantities of government assets, sometimes informally referred to as “government bonds,” central banks may further tighten financial conditions. In order to make things easier to understand, we will focus on US government securities in this part, although the concepts apply to any central bank. When a bond is sold, the investor or buyer must part with their money, which the central bank essentially removes from the system for a considerable amount of time.

CONTRACTIONARY MONETARY POLICY’S EFFECT

Economic activity and inflation are both decreased under contractionary monetary policy.

1) Impact of Higher Interest Rates: When borrowing becomes more costly in an economy, large-scale capital projects and overall spending tend to slow down. On a personal level, rising mortgage payments reduce homeowners’ discretionary income.

The increased opportunity cost of spending money is another contractionary result of rising interest rates. In a climate of growing interest rates, savings opportunities increase, making interest-linked assets and bank deposits more alluring to investors. Inflation must still be considered, however, since if it is larger than the nominal interest rate, savers will still get a negative real return.

2) The Impact of Raising Reserve Requirements: Reserve requirements may be changed to limit the amount of money available in the economy while also serving as a pool of liquidity for commercial banks in times of crisis. The quantity of loans that banks may offer will be directly reduced when central banks increase reserve requirements in response to an overheated economy, compelling banks to keep back more capital than they previously did. As anticipated, lesser economic activity results from higher interest rates coupled with fewer loans being made available.

3) The Impact of Open Market Operations (Mass Bond Sales): US Treasury securities have varying maturities and interest rates (‘T-bills’ mature in 4 weeks to 1 year, ‘notes’ in 2 to 10 years, and ‘bonds’ in 20 to 30 years). As the closest thing you can find to a “risk-free” investment, Treasury bonds are often used as benchmarks for loans with matching time horizons. For example, a 30-year mortgage may be issued with an interest rate that is higher than the benchmark to account for risk.

Bond prices are reduced when large quantities of bonds are sold, which also increases the yield on the bonds. The government will need to limit any excessive expenditure since a higher yielding Treasury instrument (bond) makes borrowing money more costly.

CONTRACTIONARY MONETARY POLICY EXAMPLES

Although there are many external factors that might affect the result of contractionary monetary policy, it is simpler in principle than it is in reality. Because of this, central bankers try to be quick-thinking, provide themselves choices to deal with unforeseen consequences, and often adjust to various circumstances using a “data-dependent” strategy.

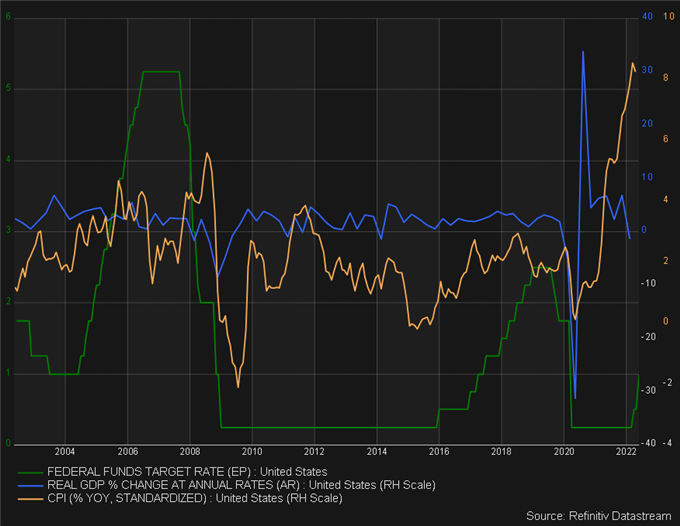

The US interest rate (Federal funds rate), real GDP, and inflation (CPI) during a 20-year period when contractionary policy was used twice are included in the example below. It’s important to keep in mind that inflation often follows the process of rate rises, which is because rate increases take time to take impact in the economy. As a result, throughout the period of May 2004 to June 2006, inflation actually maintained an upward trend while rates increased until ultimately going downward. The similar pattern was seen between December 2015 and December 2018.

In all of these instances, two distinct crises caused the whole financial system to become unstable, preventing contractionary monetary policy from being able to fully take effect. The global financial crisis (GFC) occurred in 2008/2009, and the coronavirus outbreak in 2020 shook markets and caused lockdowns that almost immediately froze international commerce.

These instances highlight how difficult it is to implement contractionary monetary policy. It’s true that the epidemic was a worldwide health emergency, but the GFC sprang from greed, financial wrongdoing, and regulatory shortcomings. The most crucial lesson from both situations is that monetary policy is subject to any internal or external shocks to the financial system and does not exist in a bubble. It is comparable to a pilot flying in a controlled environment in a flight simulator as opposed to a real flight when the pilot may be required to land the aircraft in a severe crosswind of 90 degrees.