“Compound interest is the world’s eighth marvel. Whoever comprehends it earns it; whoever does not pays it. Einstein, Albert

Since this subject has many different aspects, I’ll limit my discussion to the trading industry and the benefits of compounding returns. Any traded financial market is affected by this.

Let’s first look at two straightforward money management strategies that a trader might include in their trading plan.

- Fixed-size trades (monetary)

- Trade size in percentage (proportional to trading balance)

The first choice would imply that no matter the result of the prior transaction (win or loss), the same set monetary deal size would remain on all future trades. So how would this relate to a successful trader?

Assuming Sam and Ben, two traders, have the same approach and balance:

- $10,000 as a deposit

- Fifty-five percent of games are won.

- The average win to average loss is a profit ratio of 1.2.

Although the data above is sparse, it provides a foundation to build a visual depiction of the increase in each trader’s account.

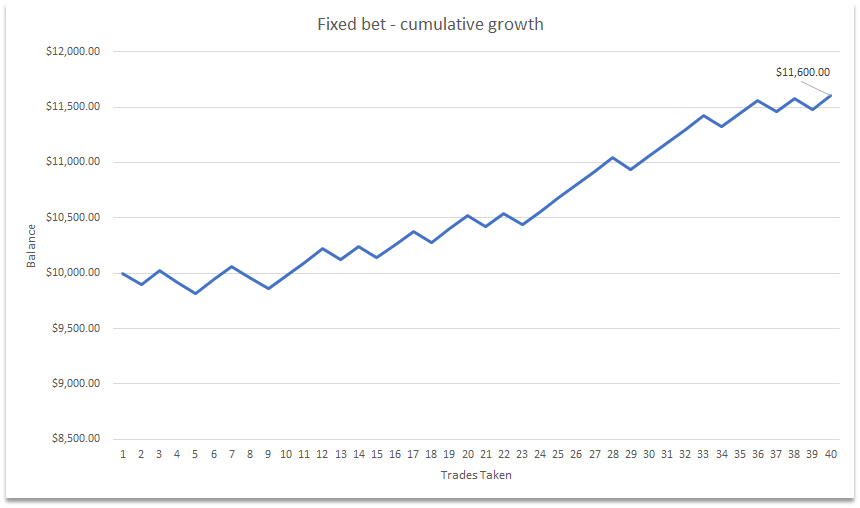

Their performance of Sam is simulated in the graph below using a FIXED Transaction SIZE of $100 for each trade he does (i.e., each loss will cost him $100):

A little side comment is necessary here. Here is only one simulation of how a line chart may display the distribution of wins and losses. Remember that there was a chance we might have had a losing result. We never know how each deal will turn out when we trade the markets and when a run of losses will start. Instead, the longer we trade, the more money we should make.

Returning to the main topic, we can observe that this produced a +16 percent increase by dividing (end balance less start balance) by end balance using the set transaction sizes discussed above.

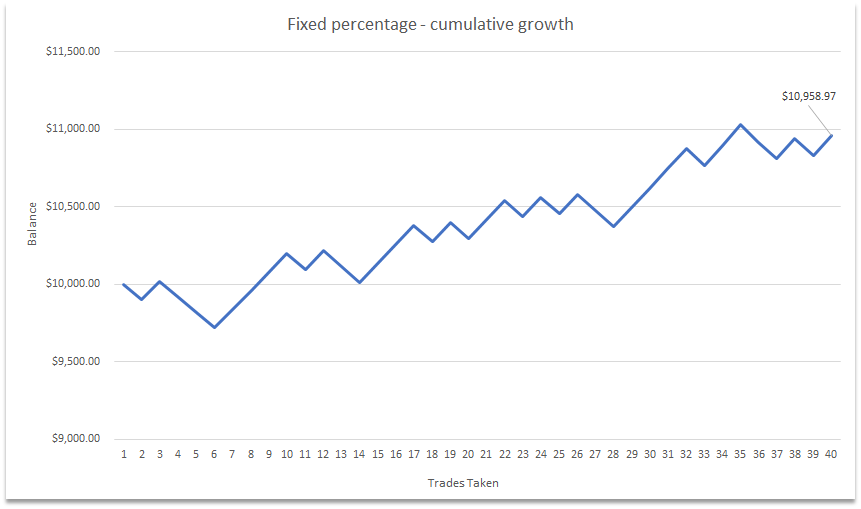

Let’s now evaluate Ben’s trading strategy, which was predicated on a FIXED PERCENTAGE of his balance. Ben will initiate his transaction with a balance of $100, and the fixed percentage will be 1 percent of that amount:

Ben has yielded (or produced) a +9.58 percent increase throughout this simulation of 40 transactions using 1% of his available balance at the time of each deal.

So, why does the set stake size on each transaction appear preferable after all?

If you still believe that, allow me to educate you.

As I mentioned before, these are short simulations, or what statisticians would call a “sample size,” and they don’t always represent what can be accomplished “over the long run.”

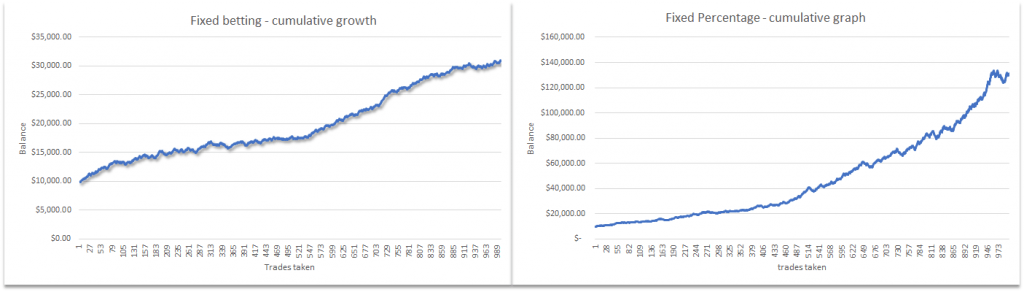

Now let’s evaluate the potential outcomes of 1,000 transactions using both betting methods side by side:

The comparable results are as follows:

- Betting System: +208.6 percent

- 1,211.5 percent as a fixed percentage

In the short term, Sam has been shown to provide a little higher return than Ben, but over the long run, Ben has progressed to purchasing his yacht while Sam is still in his row boat. One compounded his riches, while the other did not, which was the sole difference between them.

I think it’s clear that this post has two lessons. I put the potential of compounding returns front and center using a set percentage risk for every transaction. I also hope you’ve learned that it’s not always a good idea to judge if your method has a positive “expectancy,” which suggests it’s likely to withstand the test of time by looking at a few transactions.