Markets are agitated by “supply cut” comments before inventory data. In an interview with Bloomberg, the Saudi energy minister said that OPEC+ has the resources to handle oil market difficulties, including production restrictions. As soon as the markets reacted, the prices of WTI and Brent soared by 1% and 0.8%, respectively. As summer comes to a close, US drivers can now breathe a lot easier at the petrol pumps thanks to gradually falling gas prices (US driving season). WTI trades just below the pre-invasion level of $93, even if prices have dropped.

Technical levels for WTI

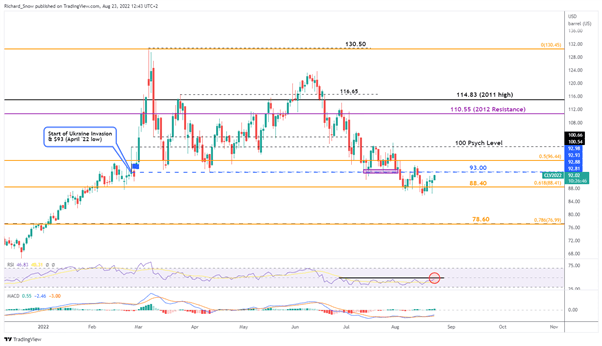

As seen by the prolonged lower wick in yesterday’s daily candle, comments from the Saudi energy minister seem to have contributed to the creation of a low of 85.75 with a quick rejection of lower pricing.

The short-term advance is now trading slightly below the pre-invasion level of approximately 93 (Russia/Ukraine), which served as support for the whole of Q2. Resistance first occurs at level 93, then at levels 96.44 and, of course, 100 psychologically.

The positive pullbacks in recent weeks have been very brief, and the RSI indicates a propensity for the indicator to reach the 50 mark before oil prices shift downward, and we are now approaching that exact same level. In order to maintain upward momentum, it will be important to contemplate a break of 93 with momentum.

Support may be found at 88.40 (61.9% Fib), then the annual low of 85.75.

Daily Chart for WTI Continuous Futures (CL1!)

SCHEDULED RISK ACTIVITIES

WTI-specific data for the week begins today with the American Petroleum Institute’s crude oil stock change and continues into tomorrow with the EIA’s crude oil stock change. On the back of last week’s 7.05 m decline in inventories, there is expected to be a drawdown of about 1.5 m in this week’s WTI-specific data.

After the consequences of demand destruction caused oil prices to trend continuously downward since July, it seems the “tight supply” story is trying to make a comeback.

The Jackson Hole Economic Symposium, which has less direct relevance to the oil market but may have broader ramifications for market mood overall, is another element to take into account near the conclusion of the week. Because of the FOMC’s recent shift away from advance guidance and toward a more data-dependent, meeting-by-meeting approach, the event has been seen by some as a spoof Federal Reserve meeting and has the potential to affect markets. On Friday, Jerome Powell, the Fed chairman, is scheduled to speak.

US Crude Oil: Retail trader data reveals that 62.61 percent of traders are net-long, with a long-to-short trader ratio of 1.67 to 1.

We normally adopt a contrarian stance to popular opinion, and the fact that traders are net long oil prices signals that they may continue to decline.

Traders who are net-long are up 0.62% from yesterday and down 22.98% from the previous week, while those who are net-short are up 2.20% from yesterday and up 41.41% from the previous week.

However, traders are less net-long today than they were yesterday and last week. Despite the fact that traders are still net-long, recent shifts in mood indicate that the current Oil – US Crude price trend may shortly reverse upward.