The nexus between economic data and financial market movements has always been undeniable. However, the US Jobs Report’s impending impact on significant assets such as gold, the US dollar, and yields promises to be a seminal moment for market participants. As the financial world holds its collective breath, delving deeper into the potential repercussions for these assets in the face of the latest labor statistics becomes paramount.

Anticipating the US Jobs Report’s Impending Impact: How the Fed’s Data-Centric Approach Alters Financial Market Dynamics

The nonfarm payrolls survey, released by the U.S. Bureau of Labor Statistics, is not just another entry in the financial calendar. It’s a litmus test for the health of the economy. With estimates suggesting that August might have seen the addition of 170,000 jobs, the weight of anticipation is palpable. What makes this even more intriguing is the Federal Reserve’s shift towards a more data-driven methodology. Depending on the robustness or frailty of the labor data, we can anticipate swings in the monetary policy that will in turn dictate the course for the U.S. dollar, yields, and gold prices in the financial markets.

At the Jackson Hole Symposium, a pivotal event in the financial world, Fed Chair Powell presented insights that are now being keenly dissected. The core message was the persistent challenge posed by inflation, which, despite the aggressive rate hikes since 2022, hasn’t been entirely tamed. However, this strong standpoint was balanced with prudence. Powell’s assertion that future actions will “proceed carefully” hinted at a steadfast commitment to ensuring decisions are informed by the most recent and relevant data.

Source: DFX

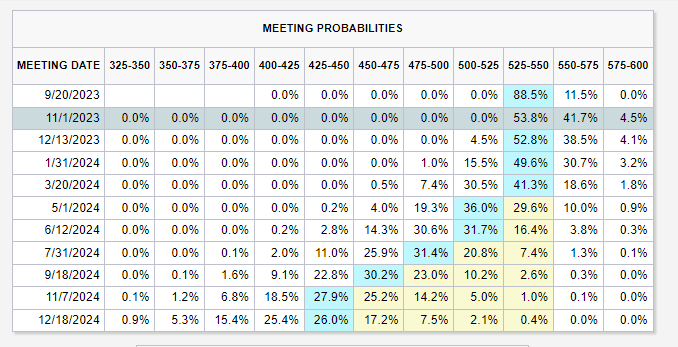

This evolving data-dependent strategy by the Fed amplifies the importance of each piece of economic information. The upcoming labor market report is not an isolated statistic; it promises to be a beacon for policy directions in the future FOMC meetings.

Analyzing the Anticipated Data Points

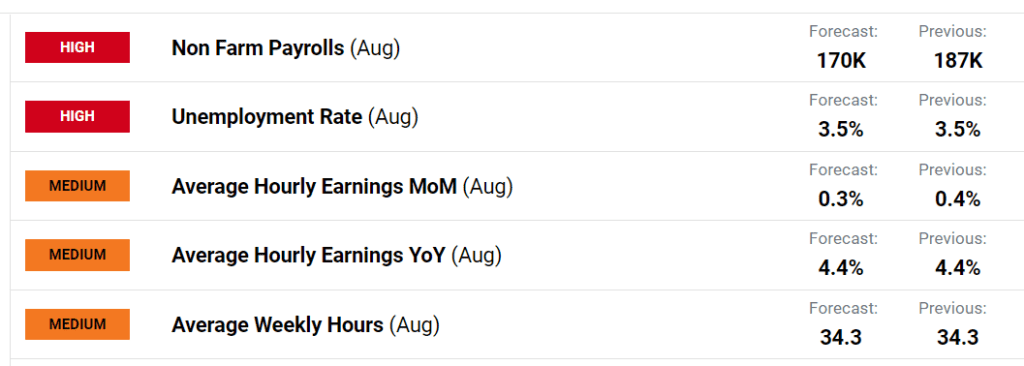

The nonfarm payrolls (NFP), always a focal point of discussions, is under the spotlight now more than ever. The forecasted growth of 170K in August, following a promising 187K uptick in July, has vast implications. Beyond the raw numbers, the underlying story of unemployment, currently pegged to remain steady at 3.5%, will be scrutinized. There’s also significant attention on the average hourly earnings, with predictions of a 0.3% monthly surge and a substantial 4.4% annual increase. Yet, this rate is somewhat in contradiction with the desired inflation target of 2.0%, presenting another intricate puzzle piece for both policymakers and investors to contend with.

Source: DFX

In the build-up to this report, a slew of economic markers have given mixed signals. Indicators such as JOLTS, consumer confidence measures, and metrics on private sector hiring haven’t showcased an overly buoyant economy. This lukewarm data suite has induced many investors to recalibrate their projections for the Fed’s future rate adjustments, pushing yields into a subdued territory. The forthcoming jobs report holds the potential to either drag these rate expectations further down or catapult them, contingent entirely on the labor market’s robustness or lack thereof.

Scenario-Based Forecasting: Unpacking the Possibilities

- Robust job gains coupled with surging average hourly earnings: If the economy showcases job gains beyond the 200,000 mark and wages experience a significant surge, the threat of heightened inflation will take center stage. A scenario of this nature might lead to considerations for further rate hikes in 2023, thereby keeping rates elevated for a more extended period. The direct financial repercussions here would likely be a strengthened U.S. dollar and heightened Treasury yields. Contrarily, assets sensitive to rates, notably gold, might find themselves under downward pressure.

- Modest employment growth and subdued average hourly earnings: The other side of the spectrum presents a different challenge. If the NFP data falls short, dipping below the anticipated 150,000 mark, and wage growth remains stagnant or even dwindles, the financial markets will be in flux. Such data would compel traders to reconfigure their assumptions on the Fed’s monetary trajectory, possibly leading to reduced bets on subsequent rate hikes. In this scenario, we could observe a dampening effect on Treasury yields and the U.S. dollar. Paradoxically, gold prices might see an uptick, considering their inverse relationship with yields.

Conclusion

The sheer magnitude of the US Jobs Report’s impending impact cannot be overstated. As data is poised to become the cornerstone of significant economic decisions, dissecting potential scenarios and preparing for a gamut of market reactions is essential for every informed investor and policymaker. With so many intricacies intertwined, the forthcoming report’s ramifications will reverberate across gold, the US dollar, and yields, setting the tone for market strategies in the near future.

Click here to read our latest article on Europe’s Struggle With Electric Car Adoption