As USD/JPY Tests Highs, BoJ Vigilantly Observes Amid Japanese Yen’s Fragile State and Global Tensions

The Japanese Yen’s Fragile State is becoming increasingly evident as global risks accelerate, casting a shadow of uncertainty over the currency markets. One currency pair that is feeling the impact of these shifts is USD/JPY, where the Japanese Yen’s weakening position is raising questions about its resilience. In this article, we will delve into the factors contributing to the Japanese Yen’s fragility and how it may affect the USD/JPY exchange rate.

The Japanese Yen, a traditionally safe-haven currency, has found itself teetering on the edge as global tensions rise. One of the primary drivers of this fragility is the escalating conflict in the Middle East, which is weighing heavily on market sentiment. Investors are seeking refuge in more stable assets, causing some to question the Yen’s ability to fulfill its historical role as a safe-haven.

Meanwhile, the US Dollar has been regaining strength, with the US Dollar Index on the rise. Treasury yields are soaring, adding to the Dollar’s allure. The benchmark 10-year Treasury note has reached its highest yield since 2007, a clear signal of investors’ growing confidence in the US economy.

One event that could further bolster the USD/JPY exchange rate is the anticipated speech by Fed Chair Jerome Powell. His remarks regarding the impact of rising bond yields on the Fed funds target rate will be closely watched. With US government bond yields surging in recent sessions, Powell’s comments could trigger heightened volatility in the currency markets.

In Japan, former Bank of Japan (BoJ) board member Makoto Sakurai believes that the central bank is more likely to abandon negative interest rates before making further adjustments to yield curve control (YCC). This perspective adds another layer of uncertainty to the Japanese Yen’s outlook, especially as yields on 10-year Japanese Government Bonds (JGB) reached their highest level since 2013.

The upcoming BoJ monetary policy meeting on October 31st will be a critical event to watch, as any hints of policy changes could have a significant impact on the Yen’s trajectory.

In the broader financial landscape, crude oil prices have eased after reaching a two-week high, partially due to the US Treasury Department’s decision to suspend sanctions on Venezuelan oil, gas, gold, and bonds. Additionally, gold has seen an uptick as diplomatic efforts in the Middle East create uncertainty and drive safe-haven flows.

The Australian Dollar faced a setback following a mixed jobs report, with the unemployment rate decreasing to 3.6% from 3.7%. However, the gains were primarily in part-time jobs, while full-time employment declined, reflecting a lower participation rate.

APAC equities followed the lead of Wall Street, with most major indices down over 1.5%. Futures indicate a challenging day ahead for equity markets in Europe and North America.

As we look ahead, the speech by Fed Chair Powell is not the only event on the calendar. The US will also release data on jobs and home sales, which could further influence the USD/JPY exchange rate.

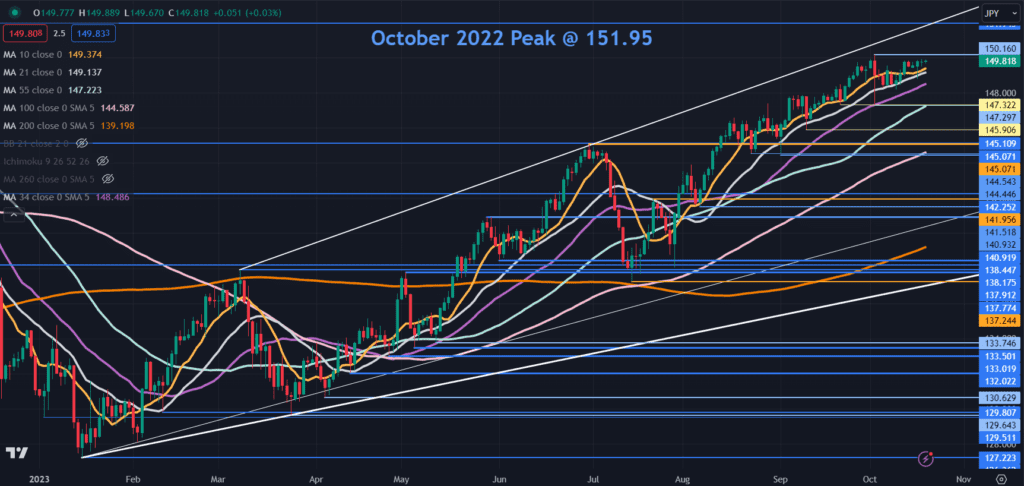

USD/JPY Technical Analysis Snapshot

USD/JPY is edging closer to the 12-month high witnessed at the start of October, currently hovering around the high of 150.16. A decisive break above this level could potentially send the currency pair toward the 33-year peak recorded last year at 151.95. However, such a move would carry the risk of intervention by the Bank of Japan (BoJ) to stabilize the exchange rate.

From a technical perspective, a bullish triple moving average (TMA) formation appears to be taking shape. This formation requires the price to be above the short-term SMA, the short-term SMA to be above the medium-term SMA, and the medium-term SMA to be above the long-term SMA, all with positive gradients. This suggests the possibility of evolving bullish momentum.

On the downside, potential support levels may lie near recent lows around 147.30 and 145.90, with further support in the 145.05 – 145.10 area and prior lows near 144.50 and 141.50.

Source: DFX

Euro’s Rally Faces Resistance, While Hawkish RBA and China GDP Affect AUD/USD, All Amidst Rising Treasury Yields

In the ever-evolving landscape of global finance, recent developments have taken center stage, influencing currency markets and commodity prices alike. The US Dollar, often regarded as a barometer for financial stability, has seen notable shifts as Treasury Yields surged to multi-year peaks. This surge in yields has sent ripples through the currency market, impacting the EUR/USD exchange rate and crude oil prices. Meanwhile, the Australian Dollar (AUD/USD) found its own path amid hawkish remarks from the Reserve Bank of Australia (RBA) and robust Chinese GDP figures.

Treasury Yields Soar, US Dollar Steadies

The US Dollar made significant strides during the Asian trading session, partially bolstered by the surge in Treasury Yields, which pushed towards multi-year highs. US retail sales data for September surprised the markets by rising 0.7% month-on-month, outperforming expectations and indicating economic resilience. The 0.6% growth seen in August added to the optimism.

Treasury yields across various maturities experienced substantial increases, with the 5- and 7-year bonds recording gains of approximately 15 basis points each. The 2-year Treasury note traded at 5.24%, a level unseen since 2006, signaling the increasing sensitivity of monetary policy to the current economic climate. Simultaneously, the benchmark 10-year note approached the 4.88% mark, its highest level since 2007.

Despite the upward pressure on yields, gold emerged as a safe haven, rallying to a 1-month peak above $1,940. The ongoing tension following a rocket attack on a Palestinian hospital, with both sides blaming each other, has contributed to the precious metal’s appeal. Crude oil also gained over 2%, partly due to the suspension of sanctions on Venezuelan oil, gas, gold, and bonds announced by the US Treasury Department.

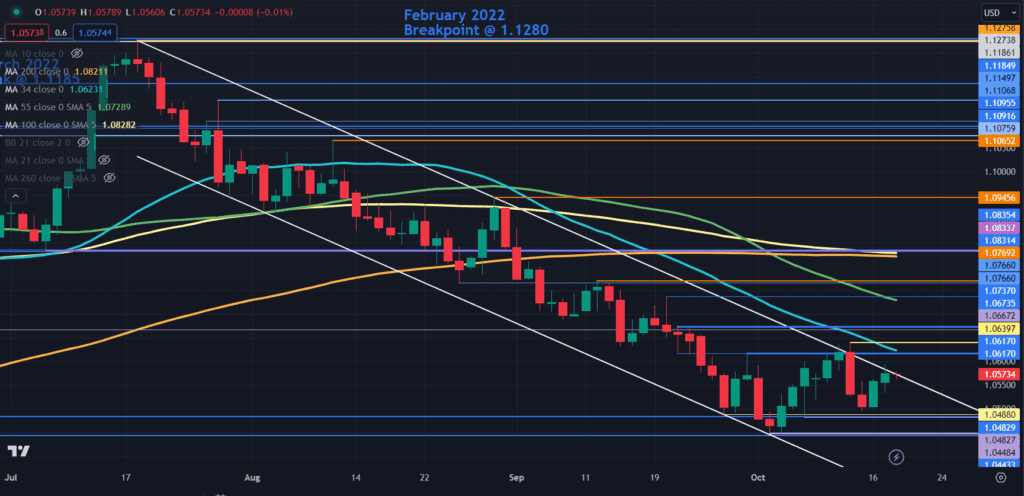

EUR/USD Faces Resistance Amidst US Dollar’s Ascendency

The EUR/USD exchange rate faced challenges as the US Dollar regained strength. The Euro’s rally encountered resistance as it tested the upper band of a descending trend channel. A clean break above this trendline could signal a pause in the overall bearish trend, possibly leading to a reversal.

Notable resistance levels for EUR/USD included the prior high near 1.0620, coinciding with the 34-day simple moving average (SMA), as well as another prior peak at 1.0673, near the 55-day SMA. Further resistance might be encountered near the 100- and 200-day SMAs near the 1.0830 mark.

On the downside, support levels appeared near the recent lows, with 1.0480 and 1.0440 serving as potential key levels. These levels had been tested recently and are worth monitoring as potential points of reference.

AUD/USD Responds to Hawkish RBA and China’s Strong GDP

The Australian Dollar (AUD/USD) found itself in the spotlight following hawkish remarks from the Reserve Bank of Australia (RBA) and impressive Chinese GDP figures. The RBA’s meeting minutes from yesterday were corroborated by RBA Governor Michele Bullock’s comments, indicating that interest rate markets have priced in a 25 basis point hike by the end of the third quarter in 2024.

China’s GDP played a pivotal role in the AUD/USD exchange rate’s movements. The 1.3% quarter-on-quarter growth for 3Q exceeded forecasts of 0.9%, along with a 0.8% prior figure. Chinese President Xi Jinping also made positive remarks about foreign investment in manufacturing, indicating a more open approach to foreign capital.

Source: DFX

Conclusion

In conclusion, the Japanese Yen’s Fragile State in the face of escalating global risks and economic factors is a central theme in the currency markets. As the USD/JPY exchange rate tests key levels, it is crucial to monitor the evolving landscape and central bank policies to gain insights into the Yen’s future trajectory. In an environment characterized by rising Treasury Yields, the US Dollar has seen increased strength, impacting currency markets and influencing commodities like gold and crude oil.

The EUR/USD exchange rate encountered resistance, with key levels to watch both on the upside and downside. Meanwhile, the AUD/USD exchange rate received a boost from a hawkish RBA and China’s robust GDP growth. As these factors continue to evolve, traders and investors are closely monitoring developments in these critical financial markets.

Click here to read our latest article on Surging Bond Volatility and Gold’s Resilient Surge