Global markets are on the edge of a significant upheaval, and it is imperative to brace for a major economic crisis. Stock markets have experienced turbulence recently, and there are signs that something much more catastrophic is on the horizon. With inflation rates soaring and central banks struggling to manage debt levels, the stability of global markets is under threat. In this article, we will delve into the key factors contributing to this looming crisis and examine what it means for investors and economies worldwide.

The Warning Signs in Global Markets

The warning signs in global markets are becoming increasingly evident. Over the past few months, stocks have shown volatility, reflecting underlying economic instability. Political opinions, often driven by emotion and media influence, have also played a role in market evaluations. Unlike rational market analyses, these opinions can cloud judgment and lead to irrational decisions. For instance, central banks have been issuing mixed signals about their ability to control inflation and manage debt levels effectively.

Furthermore, the disconnect between political narratives and economic realities is stark. Political leaders often downplay the severity of economic issues to maintain public confidence. However, this denial only postpones the inevitable reckoning that global markets will face. It is crucial for investors to remain vigilant and consider the broader implications of political decisions on economic stability.

Central Banks and Their Role

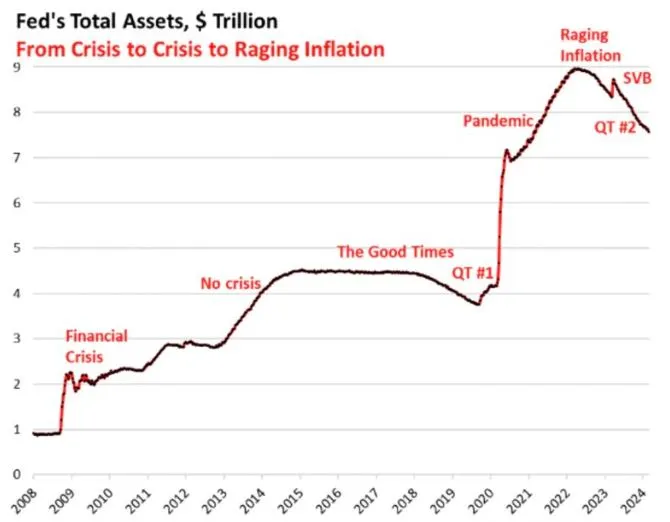

Central banks play a pivotal role in shaping the trajectory of global markets. However, their recent actions have raised concerns about long-term economic health. Many central banks have adopted short-term policies aimed at boosting immediate economic performance. This approach often involves increasing debt levels and printing more money, leading to inflation.

Thomas Hoenig, a former president of the Kansas City Federal Reserve, has criticized the short-sightedness of current central bank policies. He argues that focusing on near-term gains sacrifices long-term stability. The Federal Reserve, for instance, has prioritized bailing out banks and mitigating bond crises over ensuring sustainable economic growth. This pattern of behavior is unsustainable and poses a significant risk to global markets.

As central banks continue to manipulate interest rates and inject liquidity into the economy, the potential for an economic crisis grows. Investors must recognize the limits of these interventions and prepare for the possibility of a market correction.

The Impact of Inflation on Global Markets

Inflation is a major factor contributing to the instability of global markets. When central banks print excessive amounts of money, it devalues the currency and erodes purchasing power. This phenomenon is currently unfolding in many economies, leading to higher prices for goods and services. As inflation rises, consumers face increased financial pressure, which can dampen economic growth.

Inflation also affects investor confidence. When the value of money decreases, the returns on investments are diminished. This can lead to a decrease in market participation and a subsequent decline in stock prices. Moreover, inflation creates uncertainty, making it difficult for businesses to plan for the future. This uncertainty can result in reduced investment and slower economic growth, further exacerbating the crisis in global markets.

Debt Levels: A Ticking Time Bomb

High debt levels are another critical issue facing global markets. Many countries have accumulated significant amounts of debt in recent years, driven by expansive fiscal policies and economic stimulus measures. While these actions may provide short-term relief, they create long-term liabilities that are difficult to manage.

Rising debt levels increase the risk of default and financial instability. When governments are unable to service their debt, it can lead to a loss of confidence among investors and a sharp decline in market values. The current trajectory of debt accumulation is unsustainable, and without significant reforms, the risk of an economic crisis looms large.

Political Influence on Economic Stability

Political influence plays a substantial role in the stability of global markets. Policymakers often prioritize short-term gains and re-election prospects over long-term economic health. This behavior is evident in the way governments handle fiscal policies and debt management. By focusing on immediate political benefits, they neglect the broader impact on economic stability.

For instance, political leaders may downplay the severity of economic issues to maintain public confidence. However, this denial only postpones the inevitable reckoning that global markets will face. It is crucial for investors to remain vigilant and consider the broader implications of political decisions on economic stability.

The Future of Global Markets

The future of global markets is uncertain, with many challenges on the horizon. The interplay between inflation, central bank policies, and debt levels will significantly influence market dynamics. Investors must stay informed and be prepared to adapt to changing conditions.

In the coming months, we may witness increased volatility as markets react to new economic data and policy decisions. It is essential for investors to diversify their portfolios and consider hedging strategies to mitigate potential risks. Additionally, staying updated on global economic trends and understanding the underlying factors driving market movements will be crucial.

Preparing for the Worst

Given the current state of global markets, it is prudent for investors to prepare for a potential economic crisis. This involves reassessing investment strategies and considering alternative assets that can provide stability during turbulent times. Gold, for instance, has historically served as a hedge against inflation and economic uncertainty.

Moreover, investors should pay close attention to the actions of central banks and government policies. Understanding the potential impact of these decisions on global markets will enable investors to make informed choices and protect their assets. It is also advisable to stay diversified, balancing exposure across different asset classes to minimize risk.

Conclusion: The Road Ahead

In conclusion, global markets are on the brink of a major economic crisis. The warning signs are evident, and the factors contributing to this instability are numerous. From the actions of central banks to rising debt levels and inflation, the challenges facing global markets are significant. Investors must remain vigilant, stay informed, and be prepared to adapt to changing conditions.

While the road ahead may be uncertain, taking proactive steps to protect investments and diversify portfolios can help mitigate potential risks. By understanding the underlying factors driving market movements and staying updated on economic trends, investors can navigate these challenging times with greater confidence.

As we brace for the potential impact of this economic crisis, it is crucial to remain informed and prepared. The stability of global markets may be under threat, but with careful planning and strategic investment decisions, it is possible to weather the storm and emerge stronger on the other side.

Click here to read our latest article Exposing Federal Reserve Failures

I’m Kashish Murarka, and I write to make sense of the markets, from forex and precious metals to the macro shifts that drive them. Here, I break down complex movements into clear, focused insights that help readers stay ahead, not just informed.