The term “collapse” often conjures images of sudden and catastrophic downturns in economic systems. This article delves into how a collapse can evolve from overlooked financial practices, particularly focusing on the banking sector and its impact on the broader economy. We will explore the roles of reserves and yields in such scenarios, along with the recurrent themes of bank failure and inflation, which are central to understanding economic collapses.

The Role of Reserves in Economic Stability

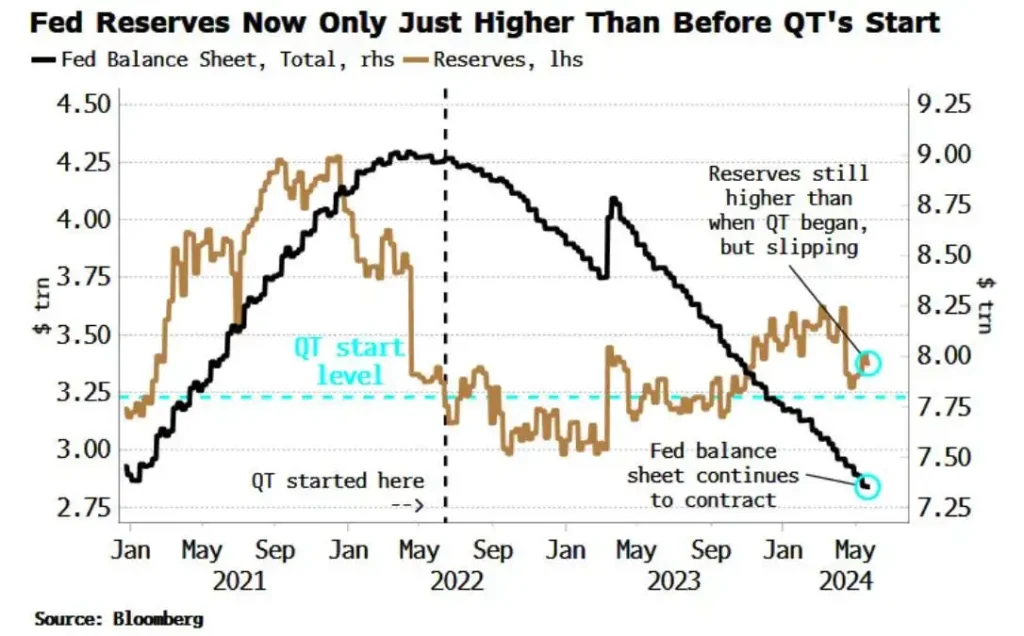

Financial reserves are crucial buffers for banks, offering a safety net in times of economic stress. Typically, a bank’s reserves help it weather periods of financial instability without resorting to drastic measures such as asset sales or requests for emergency funding. However, during a collapse, these reserves can deplete rapidly, leaving banks vulnerable to failure. This scenario was evident during recent financial crises where a depletion of reserves led directly to bank failures.

Bank reserves are directly impacted by yields on Treasury securities. As yields rise, the value of the bonds held by banks decreases. This, in turn, diminishes the overall value of their reserves. A sustained increase in yields can lead to a significant reduction in a bank’s ability to manage financial stress, pushing it towards collapse. Moreover, bank failure becomes a looming threat when reserves are insufficient to cover unexpected withdrawals or loan defaults.”

Enhancing the Resilience of Bank Reserves

The management of bank reserves is a delicate balance. Banks must carefully navigate between maintaining sufficient reserves and optimizing their financial portfolios. As the economic landscape shifts, the strategic handling of these reserves becomes more critical. Indeed, the role of reserves goes beyond mere financial safety; it serves as a linchpin for the bank’s overall health and operational continuity.

Effective reserve management involves not only adhering to regulatory standards but also anticipating future economic shifts. For example, during periods of economic prosperity, banks might be tempted to lower their reserves to increase investment activities. However, this can be risky. If the economy takes a downturn, these banks will find themselves ill-prepared for the increased withdrawals and potential loan defaults.

Furthermore, the integration of advanced analytics and financial modeling can play a pivotal role in predicting scenarios where reserves might be under stress. By employing predictive analytics, banks can foresee potential shortfalls and adjust their reserve levels accordingly. This proactive approach is essential, especially when yields are volatile and the market is unpredictable.

In addition, education and transparency about the importance of reserves can enhance stakeholder trust. Banks that openly communicate their reserve status and management strategies can build stronger relationships with their clients and investors. This transparency helps mitigate panic during economic downturns, which can further safeguard the bank’s reserves from rapid depletion.

Moreover, collaboration among banks, through forums and alliances, can foster a more stable banking environment. By sharing best practices and experiences, banks can enhance their reserve management strategies and better withstand economic pressures. This collective approach not only strengthens individual banks but also contributes to the overall stability of the financial sector.

Ultimately, the robust management of reserves is a critical defense against bank failure and economic collapse. As the financial landscape evolves, banks must remain vigilant and adaptable, ensuring that their reserves are sufficiently robust to handle future challenges.

Understanding Yields and Their Economic Impact

Yields, particularly those on government bonds, are a critical indicator of the economic environment. High yields often indicate that investors are demanding higher returns for greater perceived risks. When yields rise, it not only affects reserves but also impacts borrowing costs across the economy. Higher yields make loans more expensive, which can reduce investment and spending, further exacerbating economic decline.

In the context of a financial collapse, rising yields can accelerate the downturn by tightening financial conditions. For instance, when yields rise sharply, it can lead to a cascade of bank failures. Banks find it increasingly difficult to finance long-term investments with expensive short-term loans. This mismatch can strain their liquidity, leading to financial distress and even collapse.”

The Ripple Effects of Rising Yields on the Economy

As yields continue to climb, the broader economic implications become increasingly significant. Higher yields can dampen entrepreneurial activities by increasing the cost of capital. This scenario often discourages start-ups and small businesses from expanding or even maintaining their operations, as the cost of borrowing eclipses potential profits.

Moreover, rising yields can severely impact the housing market. As mortgage rates climb in response to higher yields, potential homebuyers may find themselves unable to afford new homes. This decrease in home buying can lead to a slowdown in the real estate market, which, in turn, affects the overall economy due to the sector’s significant economic contributions.

Additionally, governments may also feel the pinch of rising yields. Higher interest rates on government bonds mean increased costs of borrowing for public projects and services. This situation can lead to reduced government spending or higher taxes, which could further strain the economic climate.

Furthermore, the interconnection between yields and inflation is also vital. Typically, central banks might raise interest rates to combat high inflation, which directly influences yields. However, this action can also slow economic growth, creating a delicate balance for policymakers. They must navigate these waters carefully to avoid triggering a recession while trying to manage inflation.

Managing Economic Policy in High-Yield Environments

In environments where yields are high, effective economic policy becomes crucial. Policymakers must carefully consider the timing and scale of interest rate adjustments to avoid exacerbating economic challenges. Additionally, they should implement supportive measures for sectors most vulnerable to high borrowing costs, such as small businesses and housing.

Strategic fiscal policies can also cushion the blow from high yields. For instance, targeted tax relief or subsidies for small enterprises could keep them afloat and maintain employment levels during tough economic times. Similarly, investing in affordable housing projects can help stabilize the real estate market and provide much-needed economic stimulus.

Ultimately, understanding and managing the impact of yields is crucial for economic stability. By acknowledging the comprehensive effects of yields and implementing balanced policies, governments can mitigate the negative aspects of high yields and support sustainable economic growth.

Inflation: A Catalyst for Collapse

Inflation is another critical element in the dynamics of economic collapse. Persistent high inflation erodes purchasing power, leading to reduced consumer spending and economic slowdown. Moreover, inflation can complicate the monetary policy response to a collapsing economy. Central banks, faced with high inflation, may need to raise interest rates, which further increases yields and stresses financial reserves.

Repeatedly, we’ve seen how inflation can trigger a cycle that leads to bank failure. As inflation rises, central banks may increase rates to control it, inadvertently causing bond yields to spike. This increase in yields lowers the value of bank reserves, making banks more prone to failure. Thus, managing inflation is crucial to prevent a full-scale economic collapse.”

The Vicious Cycle of Inflation and Economic Pressure

Inflation’s impact extends beyond just reducing purchasing power. It also alters consumer behavior, leading to decreased demand for non-essential goods and services. This shift can ripple through the economy, causing businesses to scale back production, reduce workforce, or even shut down, which in turn leads to higher unemployment rates.

Furthermore, high inflation often forces central banks to make difficult decisions, like raising interest rates in an attempt to stabilize the currency. However, these actions, while necessary, can have unintended consequences. For instance, higher interest rates typically lead to higher borrowing costs, which can stifle economic growth and further exacerbate the conditions leading to a collapse.

In addition to impacting borrowing costs, inflation can influence the stock market adversely. Investors often flee to safer assets when inflation rises, leading to sell-offs in the stock markets. This movement can cause market volatility and diminish the value of investment portfolios, putting additional financial strain on individuals and institutions.

Strategies for Mitigating Inflation’s Impact

To combat the adverse effects of inflation, governments and central banks must implement proactive and strategic policies. One effective approach is tightening monetary policy at the right time to prevent the economy from overheating. Similarly, implementing fiscal measures to control price increases in essential goods can help manage inflation without significant negative repercussions on the economy.

Moreover, promoting economic diversification can also buffer against the impacts of inflation. By encouraging growth in various sectors, an economy can reduce its vulnerability to inflation shocks in any single industry. Additionally, enhancing economic literacy among the populace can empower consumers and investors to make informed decisions during inflationary periods, potentially stabilizing demand and investment behaviors.

In conclusion, while inflation is a complex challenge, understanding its dynamics and implementing a balanced mix of policies can mitigate its detrimental effects and prevent the cycle of economic collapse. Effective management of inflation is not just about controlling prices but also about ensuring the stability and growth of the economy in the long term.

Bank Failure: A Symptom and Cause of Economic Collapse

Bank failures are both a symptom and a cause of economic collapses. A single bank failure can erode confidence in the financial system, leading to a domino effect where more banks collapse under the pressure of a panicked financial environment. This phenomenon was observed vividly during the financial crisis of 2008, where multiple bank failures fueled a broader economic meltdown.

Moreover, the risk of bank failure escalates when banks are pressured by falling reserves and rising inflation. These elements combine to strain the financial health of banks, making them vulnerable to collapse. Therefore, preventing bank failures is pivotal in staving off a broader economic collapse.”

Cascading Effects of Bank Failures on the Economy

When a bank fails, it does not just affect the institution and its direct customers. The repercussions spread across the economy. Initially, the immediate loss of liquidity can cripple small businesses and individuals who depend on access to their funds and credit lines. This restriction in credit availability can halt business operations, leading to layoffs and reduced consumer spending.

Moreover, the uncertainty generated by a bank failure can lead to increased market volatility. Investors may begin to doubt the stability of other financial institutions, prompting a sell-off in the stock market. This loss of investor confidence can depress market values and reduce the availability of capital for other banks and businesses, further exacerbating the financial turmoil.

Furthermore, when banks are squeezed by diminishing reserves and the pressure of inflation, they may tighten lending criteria. This conservatism restricts economic growth as companies and consumers find it harder to finance new ventures or purchases. Additionally, higher interest rates meant to combat inflation can compound these challenges, making loans even more expensive and less attractive.

Strengthening Bank Resilience to Prevent Failures

To mitigate the risk of bank failures, regulatory bodies must ensure that banks maintain adequate reserves. These reserves are crucial for absorbing sudden losses and supporting the bank during financial stress. Regular stress testing can help identify potential weaknesses in a bank’s financial structure before they lead to failure.

Additionally, clear and transparent communication from banks and regulators can help restore public confidence during times of financial uncertainty. If customers feel informed and reassured about the safety of their deposits, they are less likely to participate in bank runs that can precipitate collapses.

Moreover, diversifying the services and investments of banks can also spread risk. By not putting all their financial eggs in one basket, banks can avoid catastrophic losses from a single bad investment or loan portfolio. Similarly, international cooperation among banking regulators can provide a network of support and information sharing that strengthens the entire global banking system.

In conclusion, while bank failures can trigger and exacerbate economic collapses, proactive management of reserves, careful regulatory oversight, and strategic diversification can prevent these crises. By understanding the interconnected nature of banking and economic stability, policymakers and financial leaders can better safeguard the financial system against potential collapses.

Preventive Measures and Future Outlook

To prevent economic collapse, policymakers must focus on maintaining robust reserves in banks and controlling inflation. Monitoring yields and adjusting monetary policy proactively can also help mitigate the risk of collapse. It is essential for regulators to ensure that banks have sufficient reserves to handle potential crises and to implement measures that control inflation effectively.

Furthermore, learning from past instances of collapse and adapting regulatory frameworks can help avert future crises. By understanding the interconnected nature of reserves, yields, bank failure, and inflation, policymakers can better prepare for and possibly prevent economic collapses.

In conclusion, the term “collapse” encapsulates various aspects of economic downturns. By focusing on key factors such as reserves, yields, bank failure, and inflation, we can gain a deeper understanding of economic collapses and devise strategies to mitigate their impacts. As we navigate through these challenging economic landscapes, it is crucial to maintain vigilance and proactive measures to safeguard our financial systems from potential collapse.

Click here to read our latest article on Is the Bull Market on the Brink?