WHAT IS DIVERSIFICATION OF THE STOCK SECTOR?

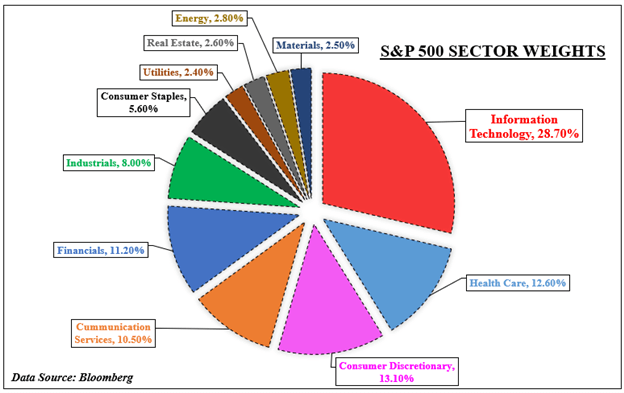

Several sectors to pick from in the S&P 500 if an investor wishes to diversify exposure to the US stock market. There are 11 options on the pie chart below, ranging from value-driven industrial businesses to information technology companies focused on growth. A trader might distribute their portfolio across any mix to insure against sector-specific hazards.

If the S&P 500 has a hiccup in this situation, losses in one market area may be countered or lessened by gains in another. This may work if the market’s various sectors aren’t dropping simultaneously. However, a stock diversification technique becomes more unreliable when practically every index component is dropping in a binary move.

This is not evidence in favor of stock diversification. Instead, market dynamics that affect how sectors in the S&P 500 move together are being examined. The CBOE Volatility Index (VIX), frequently referred to as the market’s favorite “fear gauge,” is used for this. What VIX levels should traders and investors observe because doing so risks jeopardizing their stock diversification strategy?

Sector breakdown for the S&P 500

WHAT IS THE VIX, AND WHY SHOULD TRADERS PAY ATTENTION TO IT?

To analyze volatility forecasts in the US stock market, the VIX was developed in 1990. Real-time trading occurs, representing projections for the price change over the next 30 days. As a result, its negative connection to the S&P 500 tends to be particularly strong. In other words, the VIX increases when equities decline and vice versa. You can find a detailed tutorial on the VIX here if you want to learn more.

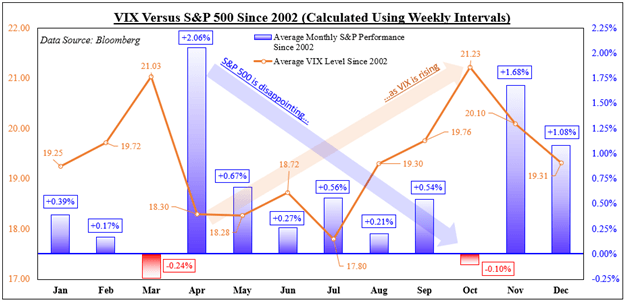

The following graph, which compares the average S&P 500 performance to corresponding VIX levels since 2002, illustrates this inverse connection. Monthly results for the research are computed using average weekly data. Doing this prevents the “volatility of volatility” from being truncated, whereas a monthly measurement might result in the data failing to capture the more significant trend.

Looking at the statistics, April typically saw the S&P 500’s most upbeat performance, averaging 2.06%. Then, this performance decreased until bottoming out in October, when the benchmark stock index returned around -0.1%. The VIX increased throughout this time, beginning at 18.30 in April and reaching 21.23 in October. Now that we know this, we can examine what occurs inside the S&P 500.

VIX COMPARED TO THE S&P 500

CORRELATIONS OF THE S&P 500 WITH THE VIX

We will require specialized price indices of the 11 sectors that make up the S&P 500 to determine when a stock sector diversification approach could fail. The latter only uses data going back to 2002. Then, on a rolling one-month basis, we can determine the correlation values between the VIX and each sector. The correlation values vary from -1 to 1. While 1 indicates perfect synchrony, a value of -1 indicates perfect inverse motions between two variables.

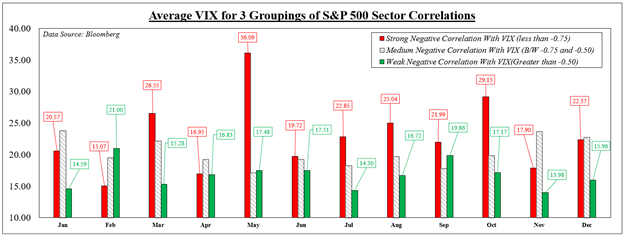

Each period’s average of all 11 results provides a cross-sector correlation reading with the VIX. Next, groups of strong (-1 to -0.75), medium (-0.75 and -0.50), and weak correlations are created (all values greater than -0.5). Strong inverse readings show the VIX rising/falling when sectors rose/fell collectively and consistently. Sectors that are weaker tend to move more freely.

Higher VIX values were linked to increased cross-sector negative correlations with the “fear gauge” in 7 out of the 12 months. When the S&P sectors moved the most in lockstep, for instance, in March, the VIX’s average weekly price was 26.55. When we saw sectors moving more freely, the price fell to 15.28—knowing this, at what VIX levels may a cross-sector diversification approach be compromised?

CROSS-SECTOR INVERSE CORRELATIONS VERSUS DIFFERENT LEVELS OF S&P PRICE VERSUS VIX

WHEN CAN A STRATEGY FOR STOCK SECTOR DIVERSIFICATION FAIL?

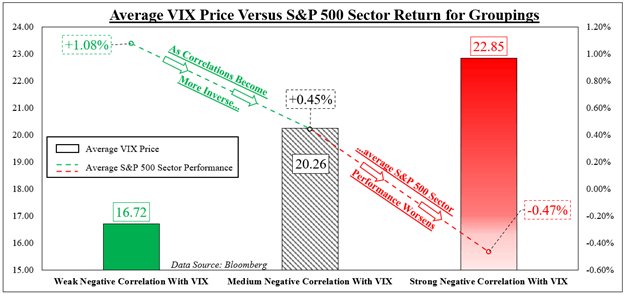

Based on the three correlation groups, we can now calculate the VIX’s average price for each month and year since 2002. We will simultaneously average the weekly performance across all S&P sectors and align them according to the same classifications. The conclusion was somewhat foreseeable, as seen by the graphic below. Growingly weaker performance across sectors coincided with stronger negative correlations with the VIX.

The average price of the “fear measure” was 22.85 when all the sectors moved in the opposite direction of the VIX the greatest. The average return for each sector at that time was -0.47 percent. On the other hand, the VIX’s price was 16.72 while the sectors were moving more freely. The average return for each sector at that price was 1.08 percent.

Keep in mind that a connection does not always indicate a cause. The VIX is not the only factor driving trade dynamics across sectors because it is at some arbitrary price. Instead, it serves as a frame of reference in this situation. A confluence of fundamental variables, including monetary policy, fiscal expenditure, business forecasts, and more, is precisely what drives markets to decline in binary movements.

HOW CAN TRADERS MANAGE VOLATILITY?

What can traders do if they anticipate excessive volatility and significant cross-correlations across market sectors in light of this information? High volatility spikes are often transient and transient. These situations are when haven-oriented investments often perform best. This includes the US Dollar, which often increases when the international market is under pressure. Another is shorting stocks. Reducing exposure to ongoing and new projects is also beneficial. Combining these might aid traders in getting ready for some rocky terrain.

VIX PRICE BASED ON CORRELATION GROUPINGS VERSUS S&P 500 SECTOR PERFORMANCE