HOW DO CENTRAL BANKS DETERMINE POLICY?

Movements in the financial markets are significantly influenced by central bank policy. Central bank officials acquire, project, and analyze economic data to forecast and assess the economy’s future course and how it relates to the central bank’s policy objectives. A central bank will often take policy action in response to difficulties or divergences from the optimal course of the economy. But deciding on a central bank’s policy is more complicated than merely sending a press release announcing a change in interest rates, a modification to asset purchases, or other supporting measures. Financial market transactions are also required for the implementation of central bank policy.

The FX markets are directly and often immediately impacted by central bank actions. Central banks‘ monetary policies change throughout time, making their respective currencies more or less desirable. Any trader who can forecast what a central bank would do will have a deeper comprehension of each necessary release of economic data; therefore, comprehending the process by which central banks make such choices is a vital ability.

REQUIREMENTS AND PRICE STABILITY

Although the US Federal Reserve is the most well-known and significant central bank, its purpose goes beyond that of the typical central bank. While most central banks are only focused on the mandate for price stability, the Federal Reserve has two goals: maximum employment and price stability. Low, constant, and predictable inflation is the best way to describe price stability. The majority of central banks aim for inflation levels of approximately 2%, which are seen to be a reliable sign of robust and steady economic development. Central banks must consider a range of economic data, circumstances, and expectations while deciding on monetary policy.

THE ECONOMIC DATA

The same economic data that FX traders and other market players regularly monitor is analyzed by central banks. Some of the most important statistics that central bankers monitor while they gather to talk and decide on policy are inflation, housing, and unemployment. These metrics are crucial for measuring GDP and spotting rising or falling patterns in a sizable economy. A fantastic resource for traders to follow the same data releases that central bankers are closely watching is the DailyFX Economic Calendar.

ECONOMISTS AND PROJECTIONS

Central banks employ hundreds of economists and monitor the same economic data that market participants can access. These economists are the ideal candidates to develop the forecasts that central banks would use to make policy since they are experts in a particular discipline and are often regarded as leaders in it. Based on current data, predictions for the future, their expertise in the field, and prospective policy options, economists develop and model economic forecasts of the future trajectory of the economy.

Central banks use these models to forecast future economic trends and assess the possible effects of their policy decisions. Several central banks regularly provide summaries of their economic and policy predictions. These summaries are an excellent resource for traders who want to know how a key market participant sees the state of the economy as a whole.

FRAMEWORK

Central banks use a framework to apply the appropriate quantity of economic data and estimates to decide if policy adjustments are required. The policy framework of a central bank describes how it views the link between important economic measures and its mission, often how various economic data points will affect inflation.

The frameworks for central bank policy have changed as the global economy has changed. Simple methods and formulae that determined the appropriate interest rates based on the link between inflation and employment formerly served as the foundation for monetary policy decisions. Since then, the world has gotten far more complicated, and central banks have shifted away from this straightforward, rule-based approach to policy.

The secular trend of low interest rates and low inflation in industrialized countries is the most significant development and has the most ramifications for central bank policy. The central bank’s capacity to combat economic downturns through straightforward interest rate reductions has been undermined by the persistence of low-interest rates. Meanwhile, central banks have been forced to reconsider and revise their view of the link between employment and inflation due to low inflation despite tight labor markets and low rates.

The Federal Reserve and the ECB have reviewed their monetary policy frameworks in light of these changing tides. The Federal Reserve revealed its conclusions and new policy framework in the late summer of 2020, while the ECB’s study and conclusions are still being finalized. The Fed’s central bankers acknowledged in their statement that the link between inflation and employment had shifted to the point where the economy could now accept greater employment levels without facing an inflation danger.

The Federal Reserve recently altered its inflation objective from a symmetric 2% to an average 2% target, which means that policymakers would now accept inflation beyond 2% as long as it contributes to bringing the average up to 2%. In effect, this new framework tells the markets that the Fed will stop trying to tighten policy at the first indications of overheating and will let the economy continue to heat up.

Understanding that stronger inflation readouts and other positive economic indicators won’t prompt the Fed to tighten monetary policy proactively is a significant break from the paradigm that prevailed in the wake of the financial crisis for traders and market participants. The significance of comprehending the central bank’s structure cannot be emphasized for central bank observers and traders in general. Understanding the framework will help you make more intelligent trading decisions since you can anticipate what the market will think of the central bank after data releases.

The central bank decides after balancing new economic facts and forecasts against its conceptual framework. When rates were raised or lowered, such a choice was straightforward. However, since the financial crisis, as central banks have been more involved in assisting the financial sector and the broader economy, their toolkits have significantly increased.

POLICY TOOLS: CONVENTIONAL VS. UNCONVENTIONAL

Before the financial crisis, most central banks had a typical toolbox. These central banks would set the short-term interest rate, and reserve requirements and other measures would be used to limit bank lending. The Bank of Japan was the main exception to these basic operational instruments; it started using “unconventional” policy tools in the late 1990s as Japan battled to recover from a severe recession and deflation.

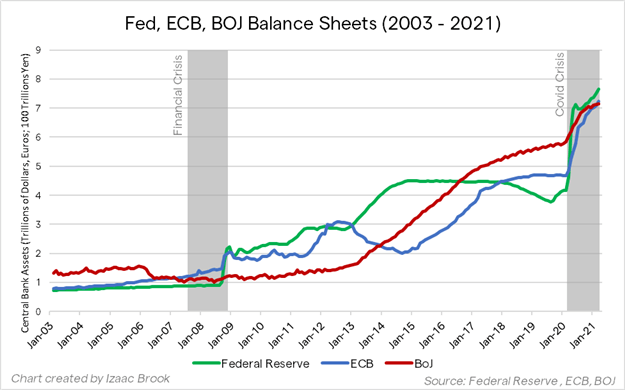

The economies of the globe were still in a state of shock following the financial crisis. Global central banks, headed by the Federal Reserve, started implementing the same radical policies pioneered by the Bank of Japan. They bought a lot of government bonds to inject a lot of liquidity into the financial system. They also decreased and maintained their policy rates at zero or even harmful levels. During the crisis, central banks also utilized their lending authority to develop new, focused mechanisms that may assist crucial components of the financial system that were not covered by conventional central bank support tools, such as money market funds and large broker-dealers.

These unorthodox instruments have grown to be a significant component of the central bank’s arsenal and have been used effectively throughout the Covid crisis. In addition to cutting policy rates back to the zero lower bound, central banks increased the breadth of their support actions beyond anything seen during the financial crisis by promising to support corporate bond markets, securing the stability of crucial components of the financial system, and buying trillions of dollars worth of government bonds.

QUANTITATIVE EASING

Central banks aimed to manipulate longer-term rates and saturate the financial system with liquidity to better support economic expenditure, growth, and inflation after the financial crisis. Quantitative easing (QE), often known as large-scale asset purchase programs, has seen central banks acquire significant amounts of government debt on the open market. Technically speaking, these activities resemble the conventional open market operations that central banks carried out before the crisis but on a considerably more extensive scale.

Although the specific mechanism of QE’s operation is still up for question, these initiatives lower longer-term interest rates, stimulate inflation, and often boost other financial markets.

Given the protracted era of low rates that leading countries have experienced, QE has also gained relevance. Since central banks can no longer reduce interest rates to the level required to kick-start the economy in a downturn, they have resorted to further QE initiatives. According to research, a program to buy assets equal to 1.5% of GDP would have a comparable effect to cutting interest rates by 25 basis points.

Before the Credit Crisis, US interest rates were just 1.50%, and rates overseas were considerably lower. Therefore, sustained QE initiatives should compensate for the shortfall in conventional rate reductions. As a result, since the Covid crisis started, asset purchase programs have grown significantly, pushing central bank balance sheets to all-time highs.

IMPLEMENTATION

The division responsible for implementing monetary policy at the central bank is in charge of implementing these unorthodox support measures. Trading and technical modifications made in the financial markets occur in the implementation division, where central bank policy is really put into practice. Head central bankers communicate their policy choices to central bank traders, who subsequently trade with particular counterparties to shift rates or implement other policy decisions.

PRE-CRISIS RATE SETTING

The Federal Reserve Bank of New York is responsible for carrying out a monetary policy on behalf of the Federal Reserve. Before the financial crisis, traders on the markets desk would be informed of the Federal Funds Rate. With main dealers, these traders would engage in open market activities.

Large banks given NY Fed approval as trading counterparties are known as primary dealers, and they are obligated to support the issue of US government debt by making markets (Treasuries). To bring short-term rates into the FOMC’s preferred range, the NY Fed markets desk would purchase or sell a certain quantity of Treasuries from these banks. This would change the amount of liquidity available in the financial system. Before the unorthodox techniques of the financial crisis were deployed, central banks around the globe used this approach of fine-tuning liquidity. When the world’s financial systems were overwhelmed with liquidity, policymaking had to advance beyond this crude technique.

POST-CRISIS RATES SETTING

Traditional open market operations would need more of an effect on liquidity and credit conditions to appreciably tighten or loosen interest rates after the QE operations carried out by central banks during the financial crisis. The rate at which banks are compensated for keeping “freshly-printed” QE money on deposit at the Fed has evolved into the Fed’s primary policy tool: interest on reserves.

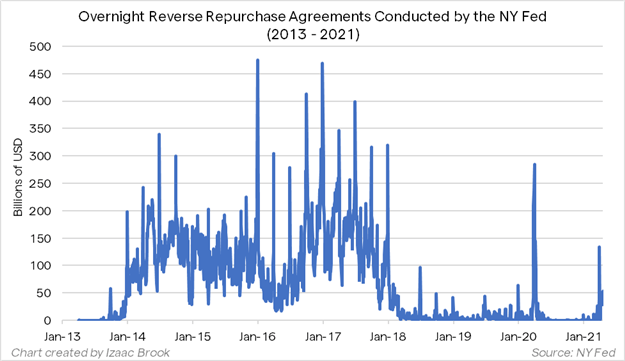

The Federal Funds Market saw a sharp decline in activity as banks stopped needing to raise money to meet regulatory obligations and stopped wanting to make unsecured loans to other banks. Interbank lending has instead moved to the repo market, where loans are backed by collateral.

The repo and reverse repo facilities offered by the NY Fed are crucial for controlling the system’s excess liquidity. Their rates are often modified with the Fed’s primary policy rate. The Fed may lend to market players looking for cash via the repo (RP) facility in exchange for Treasury collateral, which establishes an upper limit on interest rates. In contrast, the reverse repo facility (RRP) allows market parties with extra funds to borrow Treasury collateral from the Fed. The RRP facility lowers the interest rate ceiling and temporarily drains reserves from the system.

IMPLEMENTATION OF UNCONVENTIONAL POLICY

Programs for quantitative easing are carried out similarly to how open market operations operate. The central bank’s traders’ policy implementation section makes timetables and announcements outlining their intended purchases. Their counterparties provide the central bank with a list of bonds they are willing to sell, and the central bank’s traders choose and execute the most competitive offers. Although there are many memes on the internet about central banks creating money, the only physical money the central bank creates in return for these bonds is electronic. The central bank credits new digital currency to the accounts of trading counterparties.

COMMUNICATION IS IMPORTANT

Another significant addition to the central bank’s toolset since the financial crisis has been forward guidance. This is because of how the execution of monetary policy has changed. The notification of the interest rate future course is known as forward guidance. Forward guidance is based on the straightforward idea that markets, companies, and investors are constantly attempting to forecast the future movements of the central bank. Central bankers may manage expectations of their targeted objectives and provide markets more certainty by outlining their goals clearly. To apply the central bank’s perspective on essential indicators to its statement on future policy, forward guidance is linked to the policy framework.

The central bank’s communication, openness, and expectation-setting policies have developed. Since the central bank has such sway over the financial system, it is essential to uphold norms that will help it stay credible and predictable. In the wake of the financial crisis, the FOMC started to utilize forward guidance, indicating that rates would be kept at zero “for some time.” Forward guiding wording changed from a dates-based strategy to an outcomes-based one as the recovery progressed. Both strategies have been helpful for central banks throughout the globe and assist in establishing expectations for longer-term policy.

In the Covid crisis, central banks have once again sought to forward guidance to provide markets with detailed information about rate outlooks, tapering plans, and asset purchase program routes. Despite solid economic statistics and market concerns about inflation, the Federal Reserve has adhered to guidelines consistent with its new approach. Members of the FOMC have reaffirmed that rate increases and tapering won’t happen unless the Fed makes meaningful progress toward its objectives.

SUMMATION AND SETTING POLICY

Over the last twenty years, central bank policy has undergone significant change. While the data that central banks monitor to develop their policies have mostly stayed the same, how those policies are implemented has changed significantly. The emergence of secular trends in the wake of the financial crisis has also increased the need for new policy solutions. Rates and monetary policy are now more broadly controlled by central banks via the management of liquidity, extensive asset purchases, technological alterations to the money markets, and improved communication. Any trader would benefit from knowing how these elements interact, weigh in on one another, and affect the broader financial markets.