In this article, we have covered the highlights of global market news about the Australian Dollar, S&P 500, NASDAQ 100 and DOW JONES.

Forecasts for the Australian Dollar: RBA in the Fed’s Shadow for Now

The US Dollar strengthened last week in reaction to Federal Reserve Chair Jerome Powell’s much awaited speech at the Jackson Hole Symposium, making the Australian Dollar vulnerable.

Although his comments mostly met expectations, there are still some questions about his commitment to fighting inflation.

He reintroduced the exceedingly lax policies minded Alan Greenspan and Ben Bernanke nearly in the same breath as he recalled Paul Volker’s attitude of combating inflation.

It is unclear precisely where Mr. Jerome Powell stands in terms of having the guts to combat shockingly high inflation. However, in reaction, the US Dollar was purchased.

Regarding the Australian dollar, the RBA has long pointed out that the Australian economy suffers from stagnating wage growth. At a moment when they may not want it to, that might be about to change.

The minimum wage was increased by the government by 5.2% in June. A jobs conference will be held by the federal government this week, and some parties have already launched media campaigns to argue for more big salary rises.

When inflation is high and the cost of living is still rising, it is difficult to argue against salary increases.

This might potentially cause issues for the RBA in the future. A cycle of rising earnings might be sparked by significant salary rises, allowing consumers to spend more on goods and services. As a result, this raises the cost of products and services.

This compels the RBA to raise rates even higher, which raises living expenses and pressures salaries even farther upward.

The very thing that international central banks are frantically attempting to put out is this raging inferno of entrenched inflation.

The RBA could choose to play it safe as the CPI won’t be read until late October. Jumbo hikes seem to be off the table for the time being, and rate increases of 25 basis points seem like a sure thing for the sessions in September and October.

Australian dollars have recently benefited from favourable commodity prices. Due to expectations of a China comeback, the prices of iron ore, copper, and gold have increased during the last week.

The People’s Bank of China (PBOC) lowered interest rates on Monday. The interest rate on a 1-year prime loan was dropped from 3.7% to 3.65%, while the rate on a 5-year prime loan was lowered from 4.45% to 4.30%. The changes were a little bit different from the 10-basis-point expectations made by the markets for both.

Then, on Thursday, Premier Li Keqiang of the Chinese State Council unveiled another another set of stimulus measures. a 19-point plan to boost the economy with a 1 trillion Yuan (146 billion USD) budget, with an emphasis on infrastructure projects.

Although the improvement is good news, China’s economic fragility’s fundamental reasons continue. Specifically, the troubled property sector and the zero-case Covid-19 policy.

The Fed’s activities are taking precedence over RBA moves for AUD/USD. Treasury yield movements are being caused by shifts in expectations for rate rises by the US central bank, which are in turn causing US Dollar gyrations and causing the AUD/USD to fluctuate.

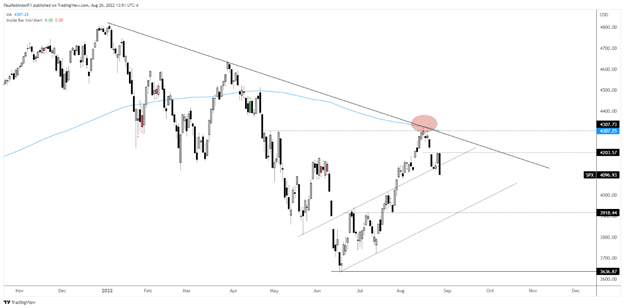

TECHNICAL FORECAST FOR S&P 500

Last week’s S&P 500 had a rough start, bounced back at Jackson Hole, but was then destroyed by Powell’s hawkish speech. This occurs when the 200-day MA and trend line were just kissed off the highs.

The idea that we are in the early stages of another significant leg down within the context of a larger bear market is strengthened by momentum that is so strong after turning off a critical position on the charts, combined with the end of summer and the impending worst portion of the year for equities.

Up until we move away lower, under 4000, there aren’t any really solid levels to monitor in terms of support. Therefore, for the time being, the market may fluctuate, but it is anticipated that rallies will be comparatively brief until a significant level is reached.

As long as the S&P remains below 4203, the short-term outlook is expected to be gloomy.

Daily S&P 500 Chart

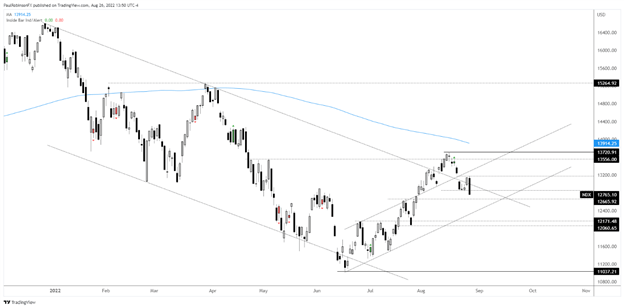

FORECAST TECHNICAL FOR NASDAQ 100

The Nasdaq 100 is once again trading within the channel that it was in at the beginning of the year, but due to this, it is struggling to establish support at previous resistance through the top channel line. Minor support may exist around 12662, but significant support won’t arrive until the 12171/60 region.

DAILY CHART OF THE NASDAQ 100

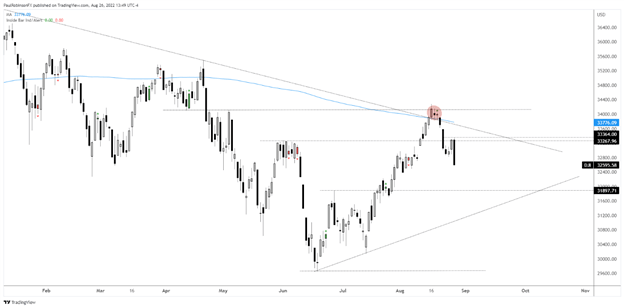

TECHNICAL FORECAST OF DOW JONES

After a small recovery, the Dow Jones is now going downward from approximately 33300. Around 31900 is the next level of support to keep an eye on. The nearest point of resistance is 33364.

DAILY CHART OF THE DOW JONES

Please click here for the Market News Updates from 26 Aug, 2022.